Gold vs. SDRs

During the lengthy discussions which led to the 1944 Bretton Woods Agreement, economist John Maynard Keynes opposed fixed exchanged rates via-a-vis a gold backed US dollar. He instead proposed the creation of a super-national unit of account which he called the bancor. The justification behind a seemingly tedious accounting unit which could be purchased in gold but not exchanged for gold nor held by individuals, was due to Keynes’s early recognition of what in the 1960s became formally identified as the Triffin Dilemma.

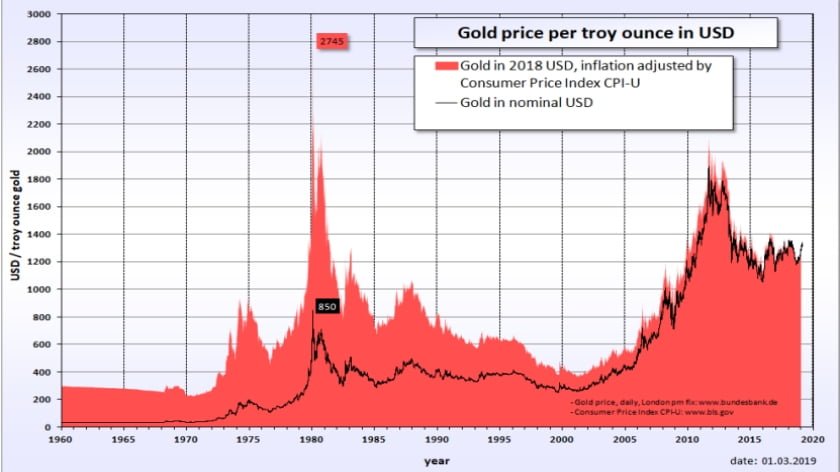

The Triffin Dilemma states that a country which issues a global reserve currency will be forced to run a current account deficit in order to provide liquidity to the wider world. In the real world this meant that a country issuing a reserve currency has to print more money than one responsibly should do in order to supply the rest of the world with a desired amount of said reserve currency. In the 1960s, this meant that the US ended up de facto devaluing the dollar by issuing more dollars than it could redeem in gold at the set rate of $35 per ounce of gold. The result was that the free market value of gold shot up and the dollar simply could not keep up.

Attempts to rectify the situation through the creation of the London Gold Pool merely delayed the inevitable. As free market gold continued to rise above the fixed rate of $35 per ounce, Richard Nixon abandoned the Bretton Woods system and ushered in the age of the fiat dollar as the world continued to ditch an overvalued dollar in exchange for gold.

In the subsequent decades after the 1971 abandonment of the imperfect Bretton Woods system, the value of the US dollar severely plummeted vis-a-vis the value of free market gold. In 2019, it requires $1,292.95 to buy a single ounce of gold that in the 1940s could be purchased with a mere $35.

Today, while the US does not have a gold standard, it does have a Triffin Dilemma nevertheless. This was pointed out after the Great Recession of 2008 by economist Zhou Xiaochuan who served as the Governor of the People’s Bank of China between 2002 and 2018. In his speech from 23 March 2009, Zhou stated:

“The Triffin Dilemma, i.e., the issuing countries of reserve currencies cannot maintain the value of the reserve currencies while providing liquidity to the world, still exists.

When a national currency is used in pricing primary commodities, trade settlements and is adopted as a reserve currency globally, efforts of the monetary authority issuing such a currency to address its economic imbalances by adjusting exchange rate would be made in vain, as its currency serves as a benchmark for many other currencies. While benefiting from a widely accepted reserve currency, the globalization also suffers from the flaws of such a system. The frequency and increasing intensity of financial crises following the collapse of the Bretton Woods system suggests the costs of such a system to the world may have

exceeded its benefits. The price is becoming increasingly higher, not only for the users, but also for the issuers of the reserve currencies. Although crisis may not necessarily be an intended result of the issuing authorities, it is an inevitable outcome of the institutional flaws”.

In this sense, the post-Bretton Woods Triffin Dilemma is even worse than that of the final decade of Bretton Woods. At least in the 1960s, American economists and politicians were aware of the problem because there was an explicit international agreement that (outside of the USA) the dollar could be redeemed for gold. Now that the dollar cannot be redeemed by anything other than the future promise of more dollars, discipline has been cast aside and the US Federal Reserve continues to issue as many dollars as it sees fit without worrying about how this trend creates outlandish levels of debt and ultimately harms the American consumer and saver.

With this in mind, Zhou Xiaochuan proposed a transition away from the US dollar towards the Special Drawing Rights (SDRs) currency basket. At present SDRs are a mixture of the value of the US dollar, Chinese Renminbi, euro, British pound and Japanese yen. SDRs cannot be held by individuals and unlike fiat currencies or gold whose value changes in real time, SDRs are revalued once every five years.

In many ways, a shift to SDRs as the major trading and reserve unit would be beneficial for the world economy. It would gradually decrease the capricious and unaccountable powers of the US Federal Reserve, it would provide a measure of stability to global trade and it would at least remove some political considerations which at present underpin the monetary policies of countries with fiat currencies. As such, it would also reduce America’s need to cause domestic inflation by printing an excess amount of dollars in order to satisfy global demand. So far – so sensible.

There are however some crucial problems with SDRs. First of all, whilst the price of gold is subject to regular fluctuation but in practice remains stable because of its intrinsic market value, SDRs remain stable on an artificial bases as its value is only changed once every five years.

As such, SDRs may well be subject to the economic phenomena known as Gresham’s law. Gresham’s law is based around the simple truth that “bad money drives out good”. In his book The Case For Gold Dr. Ron Paul explains how Gresham’s Law works in the real world in the following way:

“Unfortunately, by establishing bimetallism, Britain became perpetually subject to the evils known as Gresham’s Law, which states that when government compulsorily overvalues one money and undervalues another…

…In 17th-and 18th-century Britain, the government maintained a mint ratio between gold and silver that consistently overvalued gold and undervalued silver in relation to world market prices, with the resultant disappearance and outflow of full-bodied silver coins, and an influx of gold, and the maintenance in circulation of only eroded and ‘lightweight’ silver coins. Attempts to rectify the fixed bimetallic ratios were always too little and too late”.

If Britain faced such troubles with a bimetallic standard, one could imagine something similar but even more profound occurring in respect of SDRs. This is the case because SDRs do not include a stable metallic standard of any kind in the currency basket. Instead there are five different values of national currencies to contend with as opposed to just the valuations of gold and silver. Beyond this, because SDRs are only revalued once every five years, if within that period one (or more) of the five currencies that comprise the SDRs basket radically appreciates in terms of value, such a currency would be hoarded, thus making the SDRs exchange rate open for exploitation and ultimately destabilisation in the same way that Gresham’s law leads to such occurrence in respect of most bimetallic standards.

If bad money can drive out good in a bimetallic standard, there is nothing to prevent this from happening on an even larger scale in respect of SDRs. At present this problem hasn’t occurred because in reality, SDRs represent only a fraction of major international settlements with the dollar retaining its position as the de facto currency of international trade as well as maintaining its position as the go-to reserve currency.

But if SDRs become more prominent because of its clear virtues, its previously little discussed shortcomings will be exposed by Gresham’s law. Beyond this, as SDRs cannot be owned and traded by individuals, this presents a clear problem for any economic order that claims to be free and transparent.

A simple gold standard is the best way to avoid each of these problems. A genuine gold standard takes governmental decisions largely out of the equation, thus satisfying one of the main aims of both SDRs and the theoretical bancor which provided the intellectual framework for SDRs. A genuine gold standard is likewise not subject to the Triffin Dilemma because unlike in Bretton Woods, a true gold standard will see international trade settled in gold rather than in a proxy currency pegged to gold as was the case with the dollar under Bretton Woods or the chaotic gold exchange standard (falsely claimed to be a real gold standard) that Britain pursued in the late 1920s and early 1930s.

A gold standard also avoids the perils of Gresham’s law which logically cannot apply to a singular monetary standard. Finally, gold achieves natural stability due to market forces rather than artificial forces which time and again lead to cycles of boom and bust irrespective of failed new theory after failed new theory on how to avoid boom and bust through artificial monetary controls.

Therefore, when taken as a whole, SDRs do not represent a panacea to the world’s monetary problems. Instead, at best they represent something that could guide the world through a transitional period away from over-reliance on a fiat dollar and one that could eventually transition back to a genuine gold standard. Such a transition might indeed be long, thus requiring important reforms to SDRs before becoming a major factor in the global economy. Even so, one should not lose sight of the fact that gold eliminates the problems inherent in both a gold exchange, fiat currencies and a super-national currency basket simultaneously. As such, gold remains the best possible solution to the world’s monetary woes.

By Adam Garrie

Source: Eurasia Future