How Is Money Created? Part II

In Part I of this article, we looked at some of the prevailing confusions and contradictions within the money creation concept. We also determined that understanding commercial bank money creation will, in essence, satisfy our goal of understanding how new money is created into the economy.

In order to determine how bank money is created, let’s first look at how banks lend funds to borrowers. There are several conflicting ways of describing what banks do, specifically, how they make loans. Ordinary folks, as well as many bankers and economists, think banks make loans from the deposits they collect from other clients. In other words, most of us think banks collect deposits, and then when someone asks for a loan, banks take the collected deposit and lend it to the borrower at interest. As logical and commonsensical as it may sound, this is not true.

Nevertheless, it’s perplexing that even superstar economists like former Fed chairman Ben Bernanke profess this myth to be true. In his article titled Credit in the Macroeconomy, published in the Federal Reserve Bank of New York’s Quarterly Review for Spring 93, Bernanke uses the term ‘credit creation’ quite often and explains that this concept is defined as “the process by which saving is channeled to alternative uses”, i.e. financial intermediation of savers’ deposits into loans. This assertion by Bernanke is wrong; knowingly or unknowingly, Bernanke here is stating a falsehood.

And how do we know Bernanke is stating a falsehood? Well, we don’t have to look too far to see he’s not telling the truth here. Let’s revisit the Bank of England’s website. If we pose our original question: how is money created? on the BoE website, right at the very top of the page that shows up, it says:

“Most of the money in the economy is created by banks when they provide loans.”

It goes on to say further:

“If you borrow £100 from the bank, and it credits your account with the amount, ‘new money’ has been created. It didn’t exist until it was credited to your account.”

This, they say in plain english. Rendering what Bernanke wrote about savings being channeled to facilitate loans, categorically false.

And if you’re wondering maybe it’s just a British thing, maybe it’s different in the U.S. – well, wonder no more. A 1961 publication by Federal Reserve Bank of Chicago titled Modern Money Mechanics, written by Dorothy M. Nichols, states, under the section titled Who Creates Money?:

“The actual process of money creation takes place primarily in banks.”

And then it goes on to say,

“Transaction deposits are the modem counterpart of banknotes. It was a small step from printing notes to making book entries crediting deposits of borrowers, which the borrowers in turn could “spend” by writing checks, thereby “printing” their own money.”

So, what the heck is going on? Why – when central banks state in plain language that commercial banks create money out of nothing by making loans – economists with the highest accolade strenuously perpetuate the spurious pre-existing loan money theory that says: loans are made using existing deposits? Why do giants of economics like John Maynard Keynes call anyone who proposes that banks create money out of thin air, a ‘monetary crank’?

Here’s what Lord Keynes, who’s often called ‘the godfather of modern economics’, had to say about people who believe banks create money out of nothing by lending:

“An army of heretics and cranks who’s numbers and enthusiasm are extraordinary”, and who, according to Keynes, believe in “magic and utopia” (Keynes, 1930, vol. 2, p. 215)

Now, at this point one would think: surely, there’s been empirical studies done to demonstrate what is truly going on here, right? There has to have been some conclusive experiments done to prove, once and for all, who is right and who is a mere ‘crank’, correct? Well, as mind boggling as it may sound, in the hundred years of the Federal Reserve banking system existing in the U.S., no such studies or experiments have been conducted. Until, that is, 2014; because in 2013, Richard A. Werner, an economics professor at De Montfort University and an ardent advocate of the theory that banks create money out of thin air, set out to conduct an experiment to prove this theory conclusively with empirical evidence. Werner’s 2014 paper presents the first scientific evidence in the history of banking on whether banks can create money out of nothing.

To conduct his empirical study titled Can banks individually create money out of nothing? — The theories and the empirical evidence, Werner takes out a €200,000 loan from a small, cooperating German bank called Raiffeisenbank Wildenberg e.G. He then closely examines the bank’s balance sheets subsequent to him taking out the loan. He picks a very small bank for this purpose so that the effects of the loan show up significantly. This makes the loan easy to track within the bank’s digestive system so to speak. And since all banks in the EU – from very large to very small – conform to identical European banking regulations, results from this experiment will be identical to results from any other bank in the EU.

On the outset of his paper, Werner identifies three competing theories about the mechanism by which banks perform lending. These theories are:

- Financial intermediation theory of banking: where banks serve as mere intermediaries like other non-bank financial institutions, collecting deposits that are then lent out.

- Fractional reserve theory of banking: where individual banks are mere financial intermediaries that cannot create money, but collectively they end up creating money through systemic interactions.

- Credit creation theory of banking: where each individual bank has the power to create money ‘out of nothing’ and does so when it extends credit.

He then outlines an exhaustive account of the genesis, progression and proliferation of each of the three theories. Werner concludes his theory analysis under section 2.4 Conclusion of the literature review with the following:

“Since the 1960s it has become the conventional view not to consider banks as unique and able to create money, but instead as mere financial intermediaries like other financial firms, in line with the financial intermediation theory of banking. Banks have thus been dropped from economics models, and finance models have not suggested that bank action has significant macroeconomic effects. The questions of where money comes from and how the money supply is created and allocated have remained unaddressed.

“The literature review has identified a gradual progression of views from the credit creation theory to the fractional reserve theory to the present-day ubiquitous financial intermediation theory. The development has not been entirely smooth; several influential writers have either changed their views (on occasion several times) or have shifted between the theories.”

Werner then surmises that the key effects from his €200 thousand loan to watch for in the balance sheet, once the loan is taken out, will be whether the bank actually withdraws the loan amount from other accounts — either drawing down funds from another account (as 1. Financial intermediation theory maintains) or drawing down reserves (as 2. Fractional reserve theory maintains). He further supposes, should it be found that the bank is able to credit Werner’s account with the loan amount without having to withdraw from any other internal or external account, or without transferring the money from any other source internally or externally, this would prove the bank was able to create the loan amount out of nothing. And if that is the case, then the balance sheet will expand by the same amount lent out.

Werner notes the steps of this experiment in meticulous details. He points out that when he completed the loan transaction, in the presence of the BBC film crew filming the whole process, only one accounts manager was involved in the proceedings. His paper states:

“The accounts manager (head of the credit department, Mr. Keil) was the only operator involved in implementing, booking and paying out the loan. His actions were filmed. It was noted and confirmed that none of the bank staff present engaged in any additional activity, such as ascertaining the available deposits or funds within the bank, or giving instructions to transfer funds from various sources to the borrower’s account (for instance by contacting the bank internal treasury desk and contacting bank external interbank funding sources). Neither were instructions given to increase, draw down or borrow reserves from the central bank, the central cooperative bank or indeed any other bank or entity. In other words, it was apparent that upon the signing of the loan contract by both parties, the funds were credited to the borrower’s account immediately, without any other activity of checking or giving instructions to transfer funds.

“There were no delays or deliberations or other bookings. The moment the loan was implemented, the borrower saw his current account balance increase by the loan amount. The overall credit transaction, from start to finish, until funds were available in the borrower’s account, took about 35 min (and was clearly slowed down by the filming and frequent questions by the researcher).

“Secondly, the researcher asked the three bank staff present whether they had, either before or after signing the loan contract and before crediting the borrower’s account with the full loan amount inquired of any other parties internally or externally, checked the bank’s available deposit balances, or made any bookings or transfers of any kind, in connection to this loan contract. They all confirmed that they did not engage in any such activity. They confirmed that upon signing the loan contract the borrower’s account was credited immediately, without any such steps.”

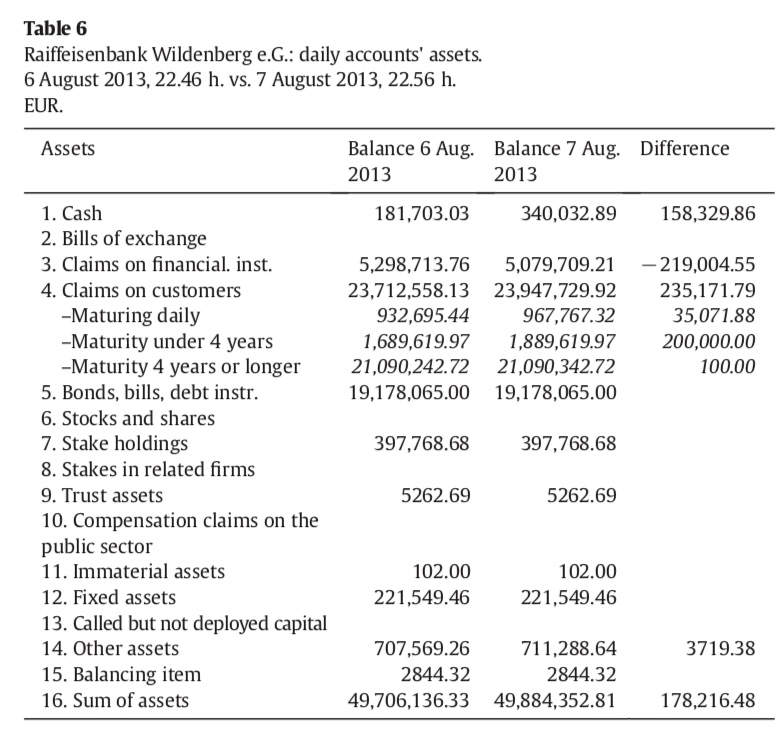

Once the process was complete, Werner obtained the bank’s daily balance sheet for the day before he took out the loan (Aug 6, 2013) and for the day the loan was disbursed (Aug 7). Next, he calculated the difference between the two balance sheets, as shown in Table 6 under section 4. Results of the paper.

As we can see in Table 6 above, following changes happened in the bank’s balance sheet between Aug 6 and Aug7 (in thousands):

- New loans that day: €235 (with Werner’s €200 plus another €35)

- Cash: +€158 (increase)

- Claims on other banks: -€219 (decrease)

- Other assets: +€4 (increase)

Resulting is an increase in Sum of Asset of +€178 for Aug 7.

So, the bank’s ‘sum of assets’ went up by €178 thousand on the day Werner took out the loan. At first glance, this asset increase of €178 thousand looks inconclusive; however, once we notice this increase also includes three other items, we realize we need to isolate the loans’ effect before drawing our conclusions.

As we note above, the €178 thousand asset increase includes three other items besides the ‘new loans’:

- Cash,

- Claims on other banks

- Other assets.

So, if we want to find out the ‘sum of asset’ change resulting from only the ‘new loans’, excluding the other three items, we need to remove (subtract) these three numbers from the stated increase in ‘sum of assets’.

Therefore, we find (in thousands):

‘Sum of assets’ increase from only the new loans = €178 – €158 – €4 – (- €219)

= €178 – €158 – €4 + €219

= €235

Meaning, when we exclude cash, other assets and claims on other banks from the Sum of assets increase on Aug 7, we find the increase in the sum of assets for the bank for that day to be €235 thousand; which matches the exact amount the bank loaned out that day.

It’s also crucial to note that, when we perform the above subtractions using the whole numbers – instead of rounding them to the nearest thousand – we get €235,171.79 increase in ‘sum of assets’ for Aug 7. This number matches – Euro to Euro, penny to penny – to the exact amount lent out that day (see Table 6 above)

So, we can clearly see there’s nothing ‘obscure’ or ‘mysterious’ about this process. Banks increase their ‘sum of assets’ by the exact amount they lend out to borrowers – plain and simple.

Therefore, Richard A. Werner’s scientific experiment establishes, with empirical evidence – for the first time in history, beyond a shadow of a doubt – that banks individually create money out of nothing. As Werner puts it:

“The money supply is created as ‘fairy dust’ produced by the banks individually, “out of thin air”.”

Furthermore, in regards to the money creation mechanism unveiled above, the Bank of England claims commercial bank’s ability to create money is kept in check by certain “capital requirements”. Clearly they’re alluding to Fractional reserve banking, but they dubiously avoid disclosing any further details on said ‘requirements’. Nevertheless, Josh Ryan-Collins, Tony Greenham and Richard Werner show in their book, titled Where Does Money Come From?, that banks’ ability to create money remains very weakly linked to the amount of reserves they hold at central banks. For example, during the 2008 financial crisis, British banks held just £1.25 in reserves for every £100 issued as credit.

Suffice it to say, the power of commercial banks to create new money has many far reaching implications. Here we have commercial banks – who are themselves private entities – creating a nation’s money supply out of thin air; and then lending it out at interest. Not only just that, banks also decide where to allocate this new money within the economy – in credit form. Impetus they face often lead them to favour lending against collateral or assets, rather than lending for investment in production. As a result, new money more often gets channelled into property and financial speculation than to small businesses and manufacturing. With profound economic consequences for society as a whole.

In fact, It doesn’t take an economist to see there’s something very wrong happening here. However, it certainly takes a clique of complicit economists to muddle the money creation concept to the point of bewilderment. So that they can turn this plain fact into some kind of ‘debate’; and then not resolve the ‘debate’ for over a century.

Indeed, it doesn’t take an expert of any kind to see signs of nefarious intent in all of this. Yet surprisingly, most of us remain oblivious. Economist J. K. Galbraith suggested why this might be:

“The process by which banks create money is so simple that the mind is repelled. When something so important is involved, a deeper mystery seems only decent.”

In conclusion, this article aimed at firmly establishing a simple truth: that commercial banks create new money in our economy out of nothing. There’s no deeper mystery to it, and we must not allow our minds to be repelled from this plain truth. Because only then can we properly address the much more significant and far more consequential questions. Questions such as:

Of all the possible alternative ways in which we could create new money and allocate purchasing power, is our current system really the best?

If not, then how do we go about changing it?

Surely the amount banks can lend is limited by regulators/ central banks, using regulatory ratios such as total loans to deposits, or to own capital (Tier One, etc). Banks create money, as you describe, but within these limits. Doesn’t the Basel agreements describe these in detail?

A few decades ago there was an extended bank strike in Ireland. Local shops accepted IOUs signed by employers. They were “money” created by non-financial, non-regulated companies. Pubs became an important and regular centre of money exchange. Some people said it was legitimate to sign the backside of your pig and pass the animal over as legal tender. Later, Dublin was set up as an Inernational Financial Services Centre. That’s when things got risky.