Is China’s Day of Reckoning Coming?

Lost in all of the geopolitical noise are some basic concepts of economics. It’s no secret that China’s economy has been built by their openly mercantilist economic policies.

Mercantilism is, oddly enough, President Trump’s dominant economic philosophy. It involves protection of domestic producers through high barriers to foreign investment and a cheap currency created through counterfeiting (we call this ‘inflation’) to boost exports of domestic products.

The problem with mercantilism is that it ultimately, like all artificial controls on the market, destroys more capital than it accumulates. Protected domestic producers already priced out of the global market and now protected from competition, have no reason to innovate and drive down costs. The government transfers wealth by stealing it through inflation from the taxpayer and subsidizing these producers through inflation.

Chinese mercantilism was allowed to go on for years because the U.S. was more than willing to subsidize their policies through equally, if not, cheaper money. We used the demand for the U.S. dollar to liquefy global trade to continually print and spend, driving up domestic prices for domestic products while sending trillions overseas to bring back rapidly depreciating consumer goods from overseas.

We are now left with a mountain of sovereign and personal debt and an equally large pile of unusable, valueless crap. In the process China ‘got rich’ off of this scheme by keeping its economy mostly closed to internal investment and deploying its insane foreign exchange reserves to encourage an equally-toxic debt mountain.

The Great Wall

They used a significant part of those funds to build out an infrastructure it sorely needed to run a modern economy serving more than a billion and a half people.

They also used a lot of that ‘wealth’ to fund a bunch of wholly uneconomic projects whose reality is being uncovered now that we’ve reached the limit of this entire Ponzi Scheme.

An article at Zerohedge has a typically-apocalyptic tone concerning the new wave of Chinese corporate defaults starting and the potential for this trickle of defaults leaking through the mercantilist dam to blow the whole thing apart.

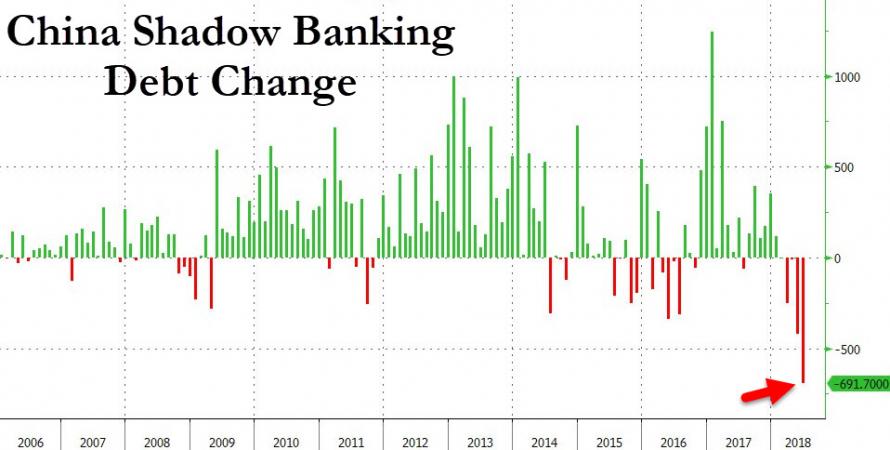

The shadow banking system is simply the system of financial transactions that happen outside of the banking system’s oversight facilities. And whenever China makes a substantive change to its monetary policy to burst another part of the shadow banking bubble these bouts of deleveraging (see chart above) occur.

There is also always a wave of bankruptcies and corporate bond defaults as well.

As it should be.

In this case it is a coal miner, Wintime Energy, who defaulted on CNY11 billion of bonds this week. There have been 18 such corporate bond defaults this year. There will likely be dozens, if not hundreds, more.

Why? Because the Trump/China trade war will take its toll on global trade. It will disrupt supplies chains, it already has. And it will cause sharper upward demand for dollars as global trade slows and debt-servicing costs for dollar-denominated corporate debt rises.

It’s becoming a gyre. And the response from China so far has been a sharp devaluation of the Yuan, more pronounced than the one in 2015 that rocked markets and set off mini-panics across commodity and then equity markets clear into Q1 2016.

Chinese Fire Drill

That is not to say, however, that some of this is not planned chaos on China’s part. It is. Since 2012, China has been trying to engineer a ‘soft landing’ of its over-levered shadow banking system.

It has not been wholly successful but it has not been an abject failure or exercise in can-kicking. Like everything else, destroying one area of the market by changing the rules begets a shift in capital to another part of the market.

In 2012/13 all the talk was about Structured Wealth Products, these were hideously-complex investment scheme which skirted banking regulations to handle the flow of hot money into China.

Then it was commodity-collateralized loans, famously stockpiling tonnes of copper to use as collateral for new loans.

Today it is equity pledging, using equities as collateral for corporate debt.

The story is always the same. Premier Xi Jinping demands a change to the shadow banking rules in some way. Defaults occur as loan servicing costs rise and liquidity dries up. The Chinese Central Bank, PBoC, then begins providing liquidity injections to the market to shore up systemically-important companies and the press in the West breathlessly tells us that China is about to explode.

Lather. Rinse. Repeat.

Now, remember, I’m not advocating this is the way the Chinese should run their economy. Or that they aren’t guilty of all the same idiocies that the U.S. and Europe are in terms of protectionism, cronyism and all the rest.

No. We are all Keynesians and Corporatists in the end, like it or not.

The question now is whether or not China has a way out of this finger-trap of escalating corporate debt?

The answer is no, but the better question is how bad will it be for them relative to everyone else dependent on China’s sustained growth?

And that is the question no one wants answered. Because a rapidly deflating shadow banking bubble in China will have knock-on effects across the entire world. And Trump’s desire to ‘balance our trade with China’ as if a trade deficit is the only way to measure relative economic activity is only exacerbating the situation.

The Bull Shop?

Trump is the new x-factor in this cycle, however. He’s not playing by the old rules and China will respond more aggressively than in the past. Don’t be surprised to see them cave on some tariff threats. Trump’s base will rejoice, thinking it’s some form of victory.

But, at the same time, as I’ve been banging my shoe on the table about for months now, China will more aggressively devalue the Yuan to maintain the losses in purchasing power of its other trading partners, emerging Asia, Central and South America, and Europe.

China’s massive buildup of wealth and imbalances in its banking system (the insane corporate debt levels) is a symptom of profligate U.S. domestic policy, which printed trillions of dollars to keep the banks alive and ran insane budget deficits to create the accounting fiction of GDP growth.

Trump is now blaming everyone else for our poor policy of exporting our debt to the world. And now the limits of all of these interactions is being reached. Capital inflows into Europe and China will reverse here in the near future and their currencies will fall.

China is already there with the Yuan. The euro is already down 8% on the year and threatening to go lower. Commodity prices are now falling, except for oil because of future supply uncertainties alone thanks to Trump.

Copper is off 15% from its Q1 high. Silver is off nearly 10%. Nickel 12%. Natural Gas 10%.

Get the picture?

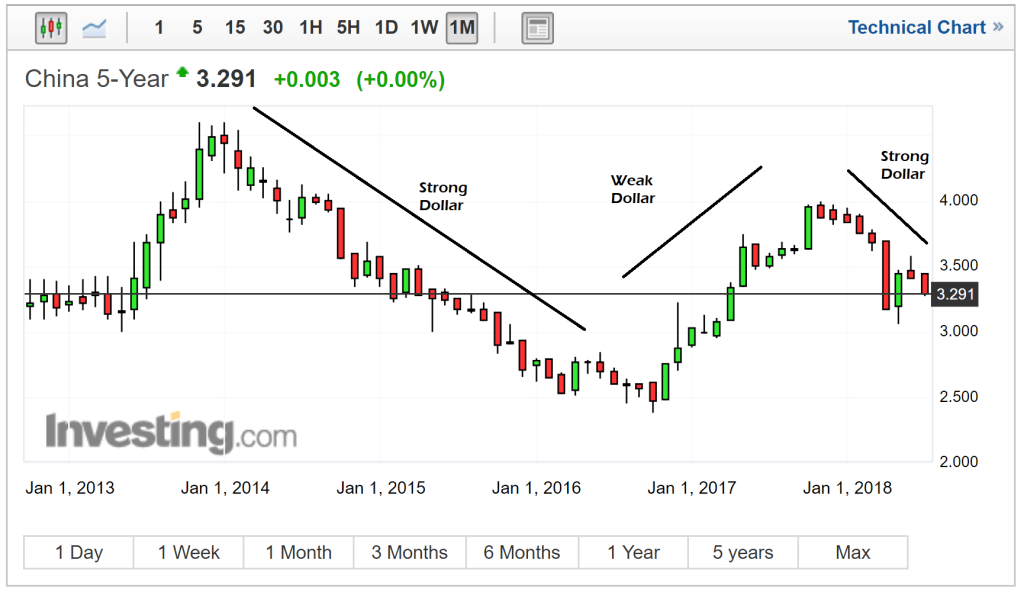

Amidst all of this the inverse relationship between China’s sovereign debt and the yuan remains.

So, there’s no loss of confidence in China’s government by investors. This is not the same as what’s happening in Turkey where Lira weakness begets bond market weakness and a spiral.

Yes, corporate bond yields are rising and spreads, as Zerohedge points out, between high-yield and investment-grade debt are widening, but there’s no panic yet, and therefore no threat of collapse.

In fact, the strong dollar and corporate debt chaos engendered by changes in policy by both Trump and Xi are giving China the opportunity to devalue and expand its sovereign debt market at improving costs. And this is because, China, smartly, has not fully opened up its capital account to allow for the money captured by their mercantilism and ours to flow back out again.

And those funds will be used, again, to bail out important companies and industries and leave the marginal ones to twist in the wind, victims of a managed creative destructionist policies of the PBoC.