Mines, Minerals, And ‘Green Energy’: A Reality Check

Summary

As policymakers have shifted focus from pandemic challenges to economic recovery, infrastructure plans are once more being actively discussed, including those relating to energy. Green energy advocates are doubling down on pressure to continue, or even increase, the use of wind, solar power, and electric cars. Left out of the discussion is any serious consideration of the broad environmental and supply-chain implications of renewable energy.

As I explored in a previous paper, “The New Energy Economy: An Exercise in Magical Thinking,”[1] many enthusiasts believe things that are not possible when it comes to the physics of fueling society, not least the magical belief that “clean-tech” energy can echo the velocity of the progress of digital technologies. It cannot.

This paper turns to a different reality: all energy-producing machinery must be fabricated from materials extracted from the earth. No energy system, in short, is actually “renewable,” since all machines require the continual mining and processing of millions of tons of primary materials and the disposal of hardware that inevitably wears out. Compared with hydrocarbons, green machines entail, on average, a 10-fold increase in the quantities of materials extracted and processed to produce the same amount of energy.

This means that any significant expansion of today’s modest level of green energy—currently less than 4% of the country’s total consumption (versus 56% from oil and gas)—will create an unprecedented increase in global mining for needed minerals, radically exacerbate existing environmental and labor challenges in emerging markets (where many mines are located), and dramatically increase U.S. imports and the vulnerability of America’s energy supply chain.

As recently as 1990, the U.S. was the world’s number-one producer of minerals. Today, it is in seventh place. Even though the nation has vast mineral reserves worth trillions of dollars, America is now 100% dependent on imports for some 17 key minerals, and, for another 29, over half of domestic needs are imported.

Among the material realities of green energy:

- Building wind turbines and solar panels to generate electricity, as well as batteries to fuel electric vehicles, requires, on average, more than 10 times the quantity of materials, compared with building machines using hydrocarbons to deliver the same amount of energy to society.

- A single electric car contains more cobalt than 1,000 smartphone batteries; the blades on a single wind turbine have more plastic than 5 million smartphones; and a solar array that can power one data center uses more glass than 50 million phones.

- Replacing hydrocarbons with green machines under current plans—never mind aspirations for far greater expansion—will vastly increase the mining of various critical minerals around the world. For example, a single electric car battery weighing 1,000 pounds requires extracting and processing some 500,000 pounds of materials. Averaged over a battery’s life, each mile of driving an electric car “consumes” five pounds of earth. Using an internal combustion engine consumes about 0.2 pounds of liquids per mile.

- Oil, natural gas, and coal are needed to produce the concrete, steel, plastics, and purified minerals used to build green machines. The energy equivalent of 100 barrels of oil is used in the processes to fabricate a single battery that can store the equivalent of one barrel of oil.

- By 2050, with current plans, the quantity of worn-out solar panels—much of it nonrecyclable—will constitute double the tonnage of all today’s global plastic waste, along with over 3 million tons per year of unrecyclable plastics from worn-out wind turbine blades. By 2030, more than 10 million tons per year of batteries will become garbage.

It’s a Material World

How much does a mile of travel or a movie weigh? Such an odd-sounding question isn’t about distance or time; instead, it points to the inescapable reality that every product and service begins with, and is sustained by, extracting minerals from the earth.

For everything built or fabricated, one can trace a straight line back upstream to where people use heavy equipment (in some countries, just shovels) to extract materials from the earth. It is obvious that there is a measurable weight in the materials used to build bridges, skyscrapers, and cars. Less obvious is the weight of materials needed to produce energy. Different forms of energy involve radically different types and quantities of energy-harvesting machines and therefore different kinds and quantities of materials.

Whether it’s liquids extracted from the earth to power an internal combustion engine or solids used to build batteries, any significant increase in materials used per mile will add up because Americans alone drive some 3 trillion road-miles a year. The same is true for delivering kilowatt-hours and all other energy uses. The upstream nature of the underlying minerals and materials needed for civilization has always been important. It is critical now that governments around the world are rushing to embrace renewable energy.

All machines wear out, and there is nothing actually renewable about green machines, since one must engage in continual extraction of materials to build new ones and replace those that wear out. All this requires mining, processing, transportation, and, ultimately, the disposing of millions of tons of materials, much of it functionally or economically unrecyclable.

Assuring access to the minerals that undergird society is a very old concern, one that is woven through history and has even precipitated wars. In the modern era, U.S. policies to address mineral dependencies date to 1922, when Congress, in the aftermath of World War I, developed a list of 42 “strategic and critical materials” for the technologies and machines important to the military at that time.[2]

Next came the Strategic Materials Act of 1939, renewed and modified several times since, incorporating ideas to encourage domestic mining and create stockpiles of strategically critical minerals for military equipment.

Over the past century, there have been two significant developments. First, the U.S. has not expanded domestic mining, and, in most cases, the country’s production of nearly all minerals has declined. Second, the demand for minerals has dramatically increased. These two intersecting trends have led to significant transformations in supply-chain dependencies. Imports today account for 100% of some 17 critical minerals, and, for 29 others, net imports account for more than half of demand.[3]

The Material Cost of “Clean Tech”

The materials extracted from the earth to fabricate wind turbines, solar panels, and batteries (to store grid electricity or power electric vehicles) are out of sight, located at remote quarries, mine sites, and mineral-processing facilities around the world. Those locations matter in terms of geopolitics and supply-chain risks, as well as in environmental terms. Before considering the supply chain, it is important to understand the scale of the material demands. For green energy, it all begins with the fact that such sources are land-intensive and very diffuse.

For example, replacing the energy output from a single 100-MW natural gas-fired turbine, itself about the size of a residential house (producing enough electricity for 75,000 homes), requires at least 20 wind turbines, each one about the size of the Washington Monument, occupying some 10 square miles of land.[4]

Building those wind machines consumes enormous quantities of conventional materials, including concrete, steel, and fiberglass, along with less common materials, including “rare earth” elements such as dysprosium. A World Bank study noted what every mining engineer knows: “[T]echnologies assumed to populate the clean energy shift … are in fact significantly more material intensive in their composition than current traditional fossil-fuel-based energy supply systems.”[5]

All forms of green energy require roughly comparable quantities of materials in order to build machines that capture nature’s flows: sun, wind, and water. Wind farms come close to matching hydro dams in material consumption, and solar farms outstrip both. In all three cases, the largest share of the tonnage is found in conventional materials like concrete, steel, and glass. Compared with a natural gas power plant, all three require at least 10 times as many total tons mined, moved, and converted into machines to deliver the same quantity of energy (Figure 1).

For example, building a single 100-MW wind farm— never mind thousands of them—requires some 30,000 tons of iron ore and 50,000 tons of concrete, as well as 900 tons of nonrecyclable plastics for the huge blades.[6] With solar hardware, the tonnage in cement, steel, and glass is 150% greater than for wind, for the same energy output.[7]

If episodic sources of energy (wind and solar) are to be used to supply power 24/7, even greater quantities of materials will be required. One needs to build additional machines, roughly two to three times as many, in order to produce and store energy when the sun and wind are available, for use at times when they are not. Then there are the additional materials required to build electricity storage. For context, a utility-scale storage system sufficient for the above-noted 100-MW wind farm would entail using at least 10,000 tons of Tesla-class batteries.

The handling and processing of such large quantities of materials entails its own energy costs as well as associated environmental implications, explored below. But first, the critical supply-chain issue is not so much the increase in the use of common (though energy-intensive) materials such as concrete and glass. The core challenges for the supply chain and the environment reside with the need for radical increases in the quantities of a wide variety of minerals.

The world currently mines about 7,000 tons per year of neodymium, for example, one of numerous key elements used in fabricating the electrical systems for wind turbines. Current clean-energy scenarios imagined by the World Bank (and many others) will require a 1,000%–4,000% increase in neodymium supply in the coming several decades.[8] While there are differing underlying assumptions used in various analyses of mineral requirements for green energy, all reach the same range of conclusions. For example, the mining of indium, used in fabricating electricity-generating solar semiconductors, will need to increase as much as 8,000%. The mining of cobalt for batteries will need to grow 300%–800%.[9] Lithium production, used for electric cars (never mind the grid), will need to rise more than 2,000%.[10] The Institute for Sustainable Futures at the University of Technology Sydney, Australia last year analyzed 14 metals essential to building clean tech machines, concluding that the supply of elements such as nickel, dysprosium, and tellurium will need to increase 200%–600%.[11]

The implications of such remarkable increases in the demand for energy minerals have not been entirely ignored, at least in Europe. A Dutch government-sponsored study concluded that the Netherlands’ green ambitions alone would consume a major share of global minerals. “Exponential growth in [global] renewable energy production capacity,” the study noted, “is not possible with present-day technologies and annual metal production.”[12]

Behind the Scenes: Ore Grades and “Overburden”

The scale of these material demands understates the total tonnage of the earth that is necessarily moved and processed. That is because forecasts of future mineral demands focus on counting the quantity of refined, pure elements needed—but not the overall amount of earth that must be dug up, moved, and processed.

For every ton of a purified element, a far greater tonnage of ore must be physically moved and processed. That is a reality for all elements, expressed by geologists as an ore grade: the percentage of the rock that contains the sought-after element. While ore grades vary widely, copper ores typically contain only about a half-percent, by weight, of the element itself: thus, roughly 200 tons of ore are dug up, moved, crushed, and processed to get to one ton of copper. For rare earths, some 20 to 160 tons of ore are mined per ton of element.[13] For cobalt, roughly 1,500 tons of ore are mined to get to one ton of the element.

In the calculus of economic and environmental costs, one must also include the so-called overburden—the tons of rocks and dirt that are first removed to get access to often deeply buried mineral-bearing ore. While overburden ratios also vary widely, it is common to see three to seven tons of earth moved to get access to one ton of ore.[14]

For a snapshot of what all this points to regarding the total materials footprint of the green energy path, consider the supply chain for an electric car battery. A single battery providing a useful driving range weighs about 1,000 pounds.[15] Providing the refined minerals needed to fabricate a single EV battery requires the mining, moving, and processing of more than 500,000 pounds of materials somewhere on the planet (see sidebar below).[16] That’s 20 times more than the 25,000 pounds of petroleum that an internal combustion engine uses over the life of a car.

The core issue here for a green energy future is not whether there are enough elements in the earth’s crust to meet demand; there are. Most elements are quite abundant, and nearly all are far more common than gold. Obtaining sufficient quantities of nature’s elements, at a price that markets can tolerate, is fundamentally determined by technology and access to the land where they are buried. The latter is mainly about government permissions.

However, as the World Bank cautions, the materials implications of a “clean tech” future creates “a new suite of challenges for the sustainable development of minerals and resources.”[17] Some minerals are difficult to obtain for technical reasons inherent in the geophysics. It is in the underlying physics of extraction and physical chemistry of refinement that we find the realities of unsustainable green energy at the scales that many propose.

| 500,000 Pounds: Total Materials Extracted and Processed per Electric Car Battery |

|---|

| A lithium EV battery weighs about 1,000 pounds.(a) While there are dozens of variations, such a battery typically contains about 25 pounds of lithium, 30 pounds of cobalt, 60 pounds of nickel, 110 pounds of graphite, 90 pounds of copper,(b) about 400 pounds of steel, aluminum, and various plastic components.(c) Looking upstream at the ore grades, one can estimate the typical quantity of rock that must be extracted from the earth and processed to yield the pure minerals needed to fabricate that single battery: • Lithium brines typically contain less than 0.1% lithium, so that entails some 25,000 pounds of brines to get the 25 pounds of pure lithium.(d) • Cobalt ore grades average about 0.1%, thus nearly 30,000 pounds of ore.(e) • Nickel ore grades average about 1%, thus about 6,000 pounds of ore.(f) • Graphite ore is typically 10%, thus about 1,000 pounds per battery.(g) • Copper at about 0.6% in the ore, thus about 25,000 pounds of ore per battery.(h) In total then, acquiring just these five elements to produce the 1,000-pound EV battery requires mining about 90,000 pounds of ore. To properly account for all of the earth moved though—which is relevant to the overall environmental footprint, and mining machinery energy use—one needs to estimate the overburden, or the materials first dug up to get to the ore. Depending on ore type and location, overburden ranges from about 3 to 20 tons of earth removed to access each ton of ore.(i) This means that accessing about 90,000 pounds of ore requires digging and moving between 200,000 and over 1,500,000 pounds of earth—a rough average of more than 500,000 pounds per battery. The precise number will vary for different battery chemistry formulations, and because different regions have widely variable ore grades. It bears noting that this total material footprint does not include the large quantities of materials and chemicals used to process and refine all the various ores. Nor have we counted other materials used when compared with a conventional car, such as replacing steel with aluminum to offset the weight penalty of the battery, or the supply chain for rare earth elements used in electric motors (e.g., neodymium, dysprosium).(j) Also excluded from this tally: the related, but non-battery, electrical systems in an EV use some 300% more overall copper used compared with a conventional automobile.(k) (a) Helena Berg and Mats Zackrisson, “Perspectives on Environmental and Cost Assessment of Lithium Metal Negative Electrodes in Electric Vehicle Traction Batteries,” Journal of Power Sources 415 (March 2019): 83–90. (b) Marcelo Azevedo et al., “Lithium and Cobalt: A Tale of Two Commodities,” McKinsey & Company, June 22, 2018; Matt Badiali, “Tesla Can’t Make Electric Cars Without Copper,” Banyan Hill, Nov. 3, 2017; Amit Katwala, “The Spiraling Environmental Cost of Our Lithium Battery Addiction,” Wired, Aug. 5, 2018. (c) Paul Gait, “Raw Material Bottlenecks and Commodity Winners,” in Electric Revolution: Investing in the Car of the Future, Bernstein Global Research, March 2017; Fred Lambert, “Breakdown of Raw Materials in Tesla’s Batteries and Possible Bottlenecks,” electrek.co, Nov. 1, 2016; Matt Bohlsen, “A Look at the Impact of Electric Vehicles on the Nickel Sector,” Seeking Alpha, Mar. 7, 2017. (d) Hanna Vikström et al., “Lithium Availability and Future Production Outlooks,” Applied Energy 110 (2013): 252–66. (e) John F. Slack et al., “Cobalt,” in Critical Mineral Resources of the United States—Economic and Environmental Geology and Prospects for Future Supply, USGS Professional Paper 1802, Dec. 19, 2017. (f) Vladmir I. Berger et al., “Ni-Co Laterite Deposits of the World—Database and Grade and Tonnage Models,” USGS Open-File Report 2011-1058 (2011). (g) Gilpin R. Robinson Jr. et al., “Graphite,” in Critical Mineral Resources of the United States. (h) Guiomar Calvo et al., “Decreasing Ore Grades in Global Metallic Mining: A Theoretical Issue or a Global Reality?” Resources 5, no. 4 (December 2016): 1–14; Vladimir Basov, “The World’s Top 10 Highest-Grade Copper Mines,” mining.com, Feb. 19, 2017; EPA, “TENORM: Copper Mining and Production Wastes”: “Several hundred metric tons of ore must be handled for each metric ton of copper metal produced.” (i) DOE, Industrial Technologies Program, Mining Industry Bandwidth Study, prepared by BCS, Inc., June 2007; Glencore McArthur River Mine, “Overburden.” The seven tons of overburden per ton of ore mined is highly variable. (j) Jeff Desjardins, “Extraordinary Raw Materials in a Tesla Model S,” visualcapitalist.com, Mar. 7, 2016; Laura Talens Peiró and Gara Villalba Méndez, “Material and Energy Requirement for Rare Earth Production,” JOM 65, no. 10 (October 2013): 1327–40. (k) Copper Development Association, “Copper Drives Electric Vehicles,” 2018. |

Sustainability: Hidden Costs of Materials

Concerns about the environmental and health effects of mining were first expressed by the ancient Greek physician Hippocrates, in his book De aëre, aquis et locis (On Air, Waters, and Places).[18] Since civilization could not exist without extracting minerals from the earth, society has long had to contend with the challenges associated with the responsible extraction of resources.

Today, the most dramatic factor driving the scale of future global mining is not the creation of products that require new uses of minerals (e.g., silicon for computers, aluminum for aircraft) but the push to use green machines to replace hydrocarbons to meet existing energy demands. Green machines mean mining more materials per unit of energy delivered to society. Since clean tech is about supplying energy in a more “sustainable” fashion, one needs to consider not just the physical mining realities but also the hidden energy costs of the underlying materials themselves, i.e., the “embodied” energy costs.

Embodied energy arises from the fuel used to dig up and move earth, grind and chemically separate minerals from the ores, refine the elements to purity, and fabricate the final product. Embodied energy costs can add up to surprising levels. For example, while an automobile weighs about 10,000 times more than a smartphone, the car requires only 400 times more energy to fabricate. And the world produces nearly 600,000 tons of consumer electronics annually.[19] Epitomizing this reality: the embodied energy to produce about 200 pounds of steel is the same as used to produce one pound of semiconductor-grade silicon.[20] The world also uses some 25,000 tons of (energy-intensive) pure semiconductor-grade silicon, a nonexistent material in the precomputer era.[21]

Embodied energy use starts with the fuel used by giant mining machines, such as the 0.3 mpg Caterpillar 797F, which can carry 400 tons of ore. There are also energy costs for electricity at the mine site (in remote areas, often diesel-powered) to run machines that crush rocks, as well as the energy costs in producing and using chemicals for refining. For minerals with very low ore grades, fuel can be a significant factor in the cost of the final product.

Rare earth elements, used in all manner of tech machines, including green ones, have rare properties but are much more abundant than gold. However, the physical chemistry of rare earths makes them difficult and energy-intensive to refine. It takes about twice as much energy to get access to and refine a pound of rare earth as a pound of lead, for example.[22]

For the mining industry, there is nothing new or surprising about the quantities of energy and chemicals used in the multistep processes needed to purify minerals locked up in rocks. While there are always ways (including, these days, with digital tools) to improve economic efficiency—and improve safety and environmental outcomes—research shows that, with regard to energy efficiency, the majority of the underlying mineral processes themselves already operate near technical or physics limits.[23]

This means that, for the usefully foreseeable future, increasing the production of green machines will unavoidably increase embodied energy. For example, analyses show that manufacturing a single battery, one capable of holding energy that is equivalent to one barrel of oil, entails processes that use the energy equivalent of 100 barrels of oil.[24] About half that energy is in the form of electricity and natural gas, and the other half oil. If the batteries are manufactured in Asia (as 60% of the world’s batteries are now), more than 60% of the electricity to do so is coal-fired.[25]

Embodied energy is also necessarily a part of building wind and solar machines, especially since large quantities of concrete, steel, and glass are required.[26] These commodity materials have relatively low embodied energy per pound, but the number of pounds involved is enormous.[27] Natural gas accounts for over 70% of the energy used to fabricate glass, for example.[28] Glass accounts for some 20% of the tonnage needed to build solar arrays. For wind turbines, oil and natural gas are used to fabricate fiberglass blades, and coal is used to make steel and concrete. Some perspective: if wind turbines were to supply half the world’s electricity, nearly 2 billion tons of coal would have to be consumed to produce the concrete and steel, along with 1.5 billion barrels of oil to make the composite blades.[29]

One additional energy factor absent from analyses of the embodied energy of clean-tech machines is in how the materials are delivered. More than 75% of all oil and 100% of natural gas are transported to markets via pipelines.[30] (Most of the remaining ton-miles take place on ships.) Pipelines are the world’s most energy-efficient means of moving a ton of material. However, nearly all the materials used to construct green machines are solids, and a very large share will be transported by truck. Using trucks instead of pipelines entails a 1,000% increase per ton-mile in the embodied transportation of energy materials.[31]

Finally, in any full accounting of environmental realities, there is the disposal challenge inherent in the very large quantities of batteries, wind turbines, and solar cells after they wear out, a subject discussed below. For now, it bears noting that many wind turbines are already reaching their 20-year end of life; decommissioning and disposal realities are just beginning. The massive, reinforced fiberglass (plastic) blades are very expensive to cut up and handle, are composed of nonrecyclable materials, and will end up in a landfill. As for solar farms, the International Renewable Energy Agency forecasts that by 2050, with current plans, solar garbage will constitute double the tonnage of all global plastic waste.[32]

For many green energy proponents, the solution to all these challenges with materials is found in a wellworn call for greater attention to “reduce, reuse, and recycle.” Many people also take refuge in the belief that our future has room in it for more energy materials because technology is “dematerializing” the rest of society. In reality, neither dematerialization nor recycling offers a solution to the heavy costs of a green energy future.

The “Dematerialization” Trope

There is a popular claim in our digital times that the increasingly service-dominated economy, combined with the Amazonification and Uberization of everything, means that “the need for resource-intensive manufacturing is not inevitable.”[33] Or, as MIT scientist Andrew McAfee put it: “For just about all of human history our prosperity has been tightly coupled to our ability to take resources from the earth. . . . But not anymore.”[34]

It is true that resource extraction—food, fuel, and minerals—accounts for only a minor share of America’s overall GDP; that has been true for more than a century. However, the foundational requirement for any of those inputs has not decreased in absolute quantity, nor has there been a diminution of the importance of the reliability and security of the supply, and price, of those inputs.

For evidence that society is not dematerializing in any fundamental way, we need only compare two iconic products of this and the past century: the smartphone and the automobile. These two products characterize a cultural shift and an apparent shift in material dependencies. As one analyst put it, teenagers have gone from driving cars to the mall to purchase music cassettes to streaming music digitally.[35] But the digital world has not eliminated the use of automobiles or the surprising quantities of minerals and materials used in the upstream production of all things digital. Forecasts for the next two decades see a 300% rise in global demand for common materials such as plastics, paper, iron, aluminum, silica (sand), and calcium (in limestone) for concrete.[36]

Wealthy economies have become more efficient, and the rate of economic growth has outpaced a slower rise in overall material use. But greater economic efficiency in material use slows the growth rate—it is not a fundamental decoupling of materials from growth. The world consumes over 100 billion tons each year in materials for construction, food, fuel, and metal parts (Figure 2).[37] That averages out to over 2 million pounds for each person’s lifetime on the planet. More than 85% of that, so far, is for nonenergy purposes.

Still, it is true that eventually—even if it is a century from now—there will be a slowing in demand for everyday materials as poorer nations approach a saturation level of per-capita use of food, homes, roads, and buildings.[38] We are a long way away from such saturation: wealthy nations have about 800 cars per 1,000 people, while in countries where billions of poorer people live, the ratio is closer to 800 people per single car.[39] To the extent that a rising share of those cars are electric, the demand for a wide variety of minerals will grow even faster.[40]

Moreover, the continual discovery of novel properties in elements drives entirely new demands for mining. A century ago, cars were manufactured using a handful of materials: wood, rubber, glass, iron, copper, vanadium, and zinc. Cars today are built from more than three dozen nonfuel minerals, including a mélange of 16 rare earth elements. One example: in 1982, a General Motors scientist employed the rare properties of neodymium to invent the world’s strongest magnet.[41] Such magnets, 10 times more powerful than anything previous, are now integral to all manner of products, including green products such as wind turbines and electric cars.

The service sector had become the primary source of employment by the end of the 20th century.[42] Most analyses and anxieties have focused on the implications of this transformation for the workforce.[43] Yet all services are also based on the use of manufactured products.[44]

There is no FedEx without trucks and aircraft; there is no health care without hospitals, magnetic imaging machines, and pharmaceuticals; there is no Amazon without data centers and warehouses. The convenience of “one-click” shopping and one- or two-day deliveries over the past half-dozen years has led to a doubling in U.S. warehouse construction and 50% rise in freight traffic.[45] Building the Cloud begins with the periodic table, from silicon and arsenic to lithium and ytterbium. Powering the Cloud requires the use of sand and steel to obtain natural gas locked up in shale, as well as silver and selenium to get solar energy.

Consider an important material-service linkage visible in energy trends. Since the start of the digital age, circa 1980, the average material intensity of America — measured in total pounds used per capita, not total pounds overall—has remained largely unchanged.[46] But the realities of how energy is used by machines, and to fabricate those machines, can be seen in the trend in energy use per industrial worker, which has increased right along with the rising share of total employment that is nonindustrial.[47] In fact, in the digitally infused period since 1980, the share of employment in services remained flat while the energy intensity of the average industrial-sector employee increased (Figure 3). In short, migration to a more service-dominated economy does not reduce dependence on energy, and derivatively materials, or the need for reliable access to both.

Reduce, Reuse, Recycle: No Exit from Mineral Dependencies

The mantra to “reduce, reuse, and recycle” ingrained in modern culture has become a feature in virtually all analyses and policy proposals directed at finding a way to reduce the materials demands of green energy. Reuse is generally irrelevant, since the vast majority of all products in society cannot be reused, and this includes green energy machines. The technical and environmental challenges, and thus the costs to reuse, more often than not are greater than those associated with using virgin material.

Reduce

Modern “reduce and recycle” policies and mandates were motivated in large measure by the goal to reduce the amount of trash going to landfills. So what will become of the rapidly increasing number of wind/ solar/battery machines that are being produced? Answer: nearly all of them will eventually show up in waste dumps.

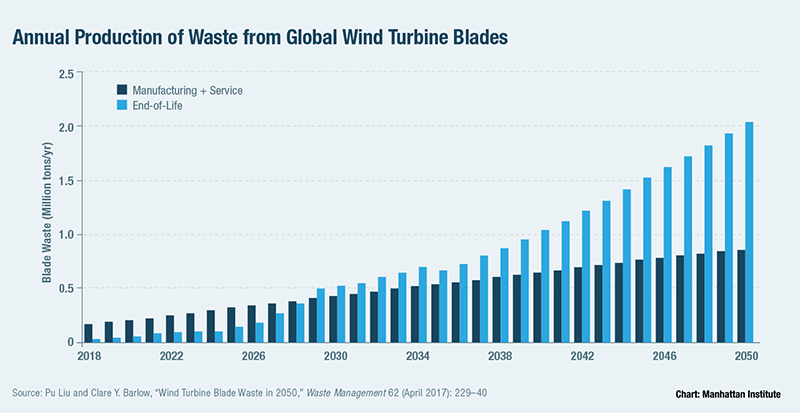

As we noted earlier, the International Renewable Energy Agency (IRENA) forecasts that by 2050, with current plans, solar garbage will constitute double the tonnage of all forms of global plastic waste. Similar scales are expected from end-of-life batteries used in electric cars and on power grids. China’s annual battery trash alone is already estimated to reach 500,000 tons in 2020. It will exceed 2 million tons per year by 2030.[48] Currently, less than 5% of such batteries are recycled.[49]

When the 20 wind turbines that constitute just one small 100-MW wind farm wear out, decommissioning and trashing them will lead to fourfold more nonrecyclable plastic trash than all the world’s (recyclable) plastic straws combined.[50] There are 1,000 times more wind turbines than that in the world today. If current International Energy Agency (IEA) forecasts are met, there will be over 3 million tons per year of unrecyclable plastic turbine blades by 2050 (Figure 4).

Recognizing the material intensity of clean energy technologies, some environmentalists suggest that what we need for a “real sustainable future is one that doesn’t involve most people driving vehicles.”[51] Proposals for encouraging or enforcing lifestyle changes are not new. They are no more likely to be effective in the future than they have been in the past.

Innovative engineering can lead to modest reductions in the use of some critical elements in electric motors and magnets. But that only slightly slows the rate of growth in demand. It doesn’t eliminate the fact that building green machines is made possible by using the properties of many specific elements. For example: samarium enables smaller and more powerful magnets that are also far more stable at high temperatures. Lithium is, tautologically, the essential element in a lithium-ion battery; and copper remains the best option for electric conductors.

Recycle

For green energy advocates, the idealized vision for recycling encompasses deploying a “circular economy” as a number-one priority for dealing with the material implications of clean tech.[52] But the idea of a green energy circular economy based on the goal of 100% recycling is a pipe dream.[53]

Many materials, especially high-value metals, can be significantly recycled. But we can consider the implications and lessons for green waste by looking at the 50 million tons of so-called e-waste generated globally from worn-out or outmoded digital devices that are also built using many critical and rare minerals. The tonnage of global e-waste equals “the weight of all commercial aircraft ever built” and is forecast to double in the next several decades.[54]

The millions of tons of e-waste contain hundreds of tons of gold and thousands of tons of silver (generally the primary target of recyclers, for obvious reasons) as well as more than a dozen other elements.[55] In order to increase e-waste recycling from today’s 20% level, the World Economic Forum (among others) proposes various measures to increase consumer “awareness,” add new regulations and subsidies, and push to redesign the original devices. The Forum estimates that these efforts would reduce consumer costs by 14% over the next two decades.[56]

But as the scale of global recycling grows, many governments and some environmental organizations are beginning to focus on the serious health and safety issues that have been ignored.[57] So far, the majority of e-waste recycling—as is much other waste—takes place in poorer nations willing to undertake the labor-intensive, largely unregulated, and sometimes hazardous processes involved. Ghana, for example, is where Europe exports the largest quantity of its e-waste.[58] Meantime, the global recycling industry is still adjusting to a new reality: two years ago, China abruptly banned the importation of waste, asserting that much of it was “dirty” and “hazardous.”[59]

China’s ban is forcing local U.S. governments and municipalities to reduce or even halt recycling programs.[60] As one industry expert in Oregon observed: “Recycling is like a religion here. . . . It has been meaningful for people in Oregon to recycle, [and] they feel like they are doing something good for the planet— and now they are having the rug pulled out from under them.”[61] The China ban has spotlighted the inherent challenges with recycling, especially the notion of a “circular economy.”

The challenge with recycling trace minerals is essentially the same as in mining itself: much depends on concentrations. The concentration of useful minerals in e-waste and green waste is very low and often far lower than the ore grades of those minerals in rocks. In addition, the physical nature of trashed hardware is highly varied (again, unlike rocks), making it a challenge to find simple mechanisms to separate out the minerals. Recycling processes are often labor-intensive (hence the pursuit of cheap labor, sometimes child labor, overseas) and hazardous because techniques to burn away unwanted packaging can release toxic fumes.[62]

If “urban mining”—the oft-used locution for capturing minerals hidden in worn-out products—were easier, cheaper, and safer than mining new materials, there would be a lot more of it, and it would not require subsidies and mandates to put into effect. While technology, especially automation and robotics, will eventually bring more economically viable and cleaner ways to recycle, the challenges are daunting and progress has been slow. That’s the reason that the overall global levels of net recycling and capture of most metals (for all purposes, not just e-waste and green waste) are below 20%, and much lower than those for all the rare earths.[63]

Even as Apple has championed recycling programs for its products—including inventing a robot to disassemble iPhones (it can only do iPhones)64 and opening a new Material Recovery Lab in Austin, Texas—the company, along with many other tech companies, vigorously promotes green energy.65 But there is as much cobalt in a single EV battery, for example, as there is in 1,000 iPhones, as much plastic in a single wind turbine as in 5 million iPhones, and as much glass in a solar array that could power a single data center as in 50 million iPhones.[66]

A recent Department of Energy vision for offshore wind (never mind onshore wind farms) in the U.S. would lead to nearly 10 thousand tons of neodymium alone “buried” inside more than 4 million tons of machinery that will eventually head for waste dumps.[67] That sounds like a lot of material worth recovering, but it pencils out to a neodymium concentration in the trash that is one-tenth of the natural ore grade for that mineral at a mine site.[68] Such realities can lead to the surprising outcome that the energy required to recover a recycled mineral can be greater than expended to get it from nature’s ore.[69]

That doesn’t mean that recycling won’t continue to have a role, even a greater one. But its limits are clear. The challenges in meeting the requirements for global minerals in the future will not be met with wishful thinking about “circular economies.”

Sources of Minerals: Conflicts and Dependencies

The critical, and even vital, roles of specific minerals have long been a concern of some analysts, and the stuff of fictional dramas as well. One plot in Amazon’s Jack Ryan series pivots around a secret Venezuelan tantalum mine; in one episode of the Netflix series House of Cards, a crisis emerges from a Chinese samarium embargo.[70] The dramas are, of course, animated by real-life dependencies and conflicts over resources, local labor abuses, and gratuitous damage to the local environment.

Today, one can trace a straight line from a medical MRI to giant trucks in the mines of Brazil (for niobium in superconducting magnets),[71] or from an electric car to Inner Mongolia’s massive Bayan Obo mines (for rare earths), and from a smartphone to mines in the Democratic Republic of Congo (for cobalt in batteries). Each of those regions represents the world’s largest supply of niobium, rare earths, and cobalt, respectively.[72] Politically troubled Chile has the world’s greatest lithium resources, although stable Australia is the world’s biggest supplier. Elsewhere in the battery supply chain, Chinese cobalt refiners have quietly gained control over more than 90% of the battery industry’s cobalt refining, without which the raw cobalt ore is useless.[73]

The Institute for Sustainable Futures at the University of Technology Sydney, Australia, cautions that a global gold rush for green minerals to meet ambitious plans could take miners into “some remote wilderness areas [that] have maintained high biodiversity because they haven’t yet been disturbed.”[74] And then there are the widely reportedly cases of abuse and child labor in mines in the Congo, where 70% of the world’s raw cobalt originates.[75]

Late in 2019, Apple, Google, Tesla, Dell, and Microsoft found themselves accused in a lawsuit filed in a U.S. federal court of exploiting child labor in the Congo.[76] Similar connections can be made to labor abuses associated with copper, nickel, or niobium mines around the world.[77] While there is nothing new about such real or alleged abuses, what is new is the rapid growth and enormous prospective demand for tech’s minerals and green energy minerals. The Dodd-Frank Act of 2010 includes reporting requirements on trade in “conflict minerals.” A recent Government Accountability Office (GAO) report notes that more than a thousand companies filed conflict minerals disclosures with the Securities and Exchange Commission, per Dodd-Frank.[78]

Automakers building electric cars have joined smartphone makers in such pledges for “ethical sourcing” of minerals.[79] Car batteries use far more of “conflict” cobalt.[80] Companies can make pledges; but unfortunately, the facts suggest that there is little correlation between such pledges and the frequency of (claimed) abuses in foreign mines.[81] In addition to moral questions about exporting the environmental and labor challenges of mineral extraction, the strategic challenges of supply chains are a top security concern as well.

Strategic Dependencies: Old Security Worries Reanimated

Supply-chain worries about critical minerals during World War I prompted Congress to establish, in 1922, the Army and Navy Munitions Board to plan for supply procurement, listing 42 strategic and critical materials. This was followed by the Strategic Materials Act of 1939. By World War II, some 15 critical materials had been stockpiled, six of which were released and used during that war. The 1939 act has been revised twice, in 1965 and 1979, and amended in 1993 to specify that the purpose of that act was for national defense only.[82]

As recently as 1990, the U.S. was the world’s number-one producer of minerals. It is in seventh place today.[83] More relevant, as the United States Geological Survey (USGS) notes, are strategic dependencies on specific critical minerals. In 1954, the U.S. was 100% dependent on imports for eight minerals.[84] Today, the U.S. is 100% reliant on imports for 17 minerals and depends on imports for over 50% of 29 widely used minerals. China is a significant source for half of those 29 minerals.[85]

The Department of Defense and the Department of Energy (DOE) have issued reports on critical mineral dependencies many times over the decades. In 2010, DOE issued the Critical Materials Strategy; in 2013, DOE formed the Critical Materials Institute, the same year the National Science Foundation launched a critical-materials initiative.[86] In 2018, USGS identified a list of 35 minerals as critical to security of the nation.[87]

But decades of hand-wringing over rising mineral dependencies have yielded no significant changes in domestic policies. The truth is that depending on imports for small quantities of minerals used in vital military technologies can be reasonably addressed by building domestic stockpiles, a solution as ancient as mining itself. However, today’s massive domestic and global push for clean-tech energy cannot be addressed with small stockpiles. The options—other than eschewing more green energy—are to simply accept more strategic dependency, or to increase domestic mining.[88]

Green Energy’s Radical Acceleration of Strategic Dependencies

The U.S. has in the past half-decade achieved strategic energy independence. This comes after decades of political, economic, and geopolitical anxieties over import dependencies for natural gas and oil, in particular. The nation now produces more gas than it consumes and is thus a net exporter; it also produces 90% of net petroleum needs and is thus essentially strategically independent. As with agricultural products, where the U.S. is also a net exporter, achieving net independence does not obviate a need for or value in imports as part of the overall complex structure of commodity exchanges. But strategic “insulation,” as well as geopolitical “soft power,” comes from a posture of “dominance” in commodities critical to national survival.[89] While it remains to be seen how much damage is inflicted on domestic energy production in the post-coronavirus recession, it is now clear that the nation has significant capabilities in strategic hydrocarbon production and exports. Given that 56% of all America’s energy comes from oil and gas, this achievement has deep strategic implications.

On the other hand, as of today, just 4% of overall domestic energy needs are supplied by wind and solar machines, and batteries propel less than 0.5% of domestic road-miles. About 90% of solar panels are imported.[90] Even if the panels were assembled here, the U.S. fabricates only 10% of the global supply of the critical underlying silicon material. China produces half.[91] For wind turbines, the U.S. imports some 80% of the electrical components (i.e., excluding fiberglass and steel).[92] And while Tesla (accounting for nearly 80% of all domestic EV sales)[93] manufactures domestically, essentially all the critical minerals originate overseas.

Thus, any significant expansion in green machines’ tiny share of domestic energy will radically increase imports of either those machines, or the green energy minerals, or both. The quantities of imports will be unprecedented.

The strategic implications of green energy materials have not escaped attention in Europe. An analysis from The Hague Centre for Strategic Studies summarized the “security dimension” of the world’s rush to promote renewable energy. The analysis points to three obvious macro trends:

- Mineral-producing countries will gain power.

- Regions with “large unexploited mineral reserves” will gain strategic importance.

- The “gravity of international relations will shift towards countries that possess renewable energy technologies and technical know-how on minerals for renewable energy.”

The Hague drily notes that “import dependent countries may use military capabilities to secure mineral resources.”[94]

As a consequence, it appears that Europe might embrace policies to encourage more domestic mining, an idea that would have seemed as unlikely a few years ago as the possibility of the EU encouraging more drilling for oil and natural gas. But that is precisely what is being proposed in a “retooling” of the EU’s industrial policy.[95] Citing strategic and economic factors, some EU policymakers propose more local mining and refining to meet the mineral needs of green energy. Potential mining projects have been identified in 10 EU countries, including rare earths in Norway, cobalt in Finland, and lithium in Spain and Portugal. It is no small irony that, as the European Investment Bank puts in place policies to stop lending to fossil fuel industries,[96] it is implementing policies to lend to mining projects.[97]

It remains to be seen how Europe’s newfound mining ambitions will be greeted by environmentalists and the continent’s various green parties, given the hostility of both to extraction industries in general. Just prior to the global coronavirus pandemic, protests started to erupt over plans for new European mines,[98] in response to which industries were spooling up a PR campaign to try to manage “the unfavourable status of mineral extraction.”[99]

In any event, environmentalists on both sides of the Atlantic continue to push harder for expanding green energy.[100] How this all plays out in the post-coronavirus world also remains to be seen. But regardless of whether green energy policies are accelerated or slow down, the significant mineral dependencies that already exist will not change unless the U.S. learns to love, or at least make peace with, more mining.

Policies for Supply-Chain Security for Energy Materials: Dig More

Several decades of studies, congressional hearings, and policy analyses have all pointed to the same two facts.[101] One, the territories of the United States contain vast mineral reserves worth trillions of dollars, including every mineral relevant to green energy machines, not to mention those critical for computers and the military.[102] Two, America’s share of domestic and global mineral supply continues to shrink.

Similarly, decades of proposals reaching back to the Strategic Materials Act of 1939 have all offered a list of action items that are, each time, essentially identical. And all have included the one central and obvious conclusion: the primary means for decreasing import dependencies is to increase domestic mining.[103] As the National Academies of Sciences pointed out in a 1999 report on mining: “lack of early, consistent cooperation and participation by all the federal, state and local agencies involved in the NEPA process results in excessive costs, delays and inefficiencies.”[104]

The U.S. has one of longest permitting processes in the world; investors must navigate a labyrinth of dozens of federal, state, and local rules.[105] It can take one to three decades to get one new mine into production.106 This compares with a permitting process that typically takes about two years in Canada and Australia.[107] (Permitting in those nations has recently become more arduous.)[108] The U.S., along with Europe, has regulated its way into far greater import dependencies.[109] Less than 10% of global spending on mineral exploration happens on U.S. soil.[110]

At the same time, policymakers and U.S. presidents over the years have radically decreased access to federal lands for mineral exploration, never mind development. In the western states where the federal government controls nearly 90% of the total land area,[111] nearly half that territory is off-limits to mining.[112] In addition, Congress in 1996 closed down America’s epicenter of mining expertise, the Bureau of Mines, laying off most of the staff and distributing those who remained to various other agencies.[113]

Last year, the Trump administration proposed to increase domestic mining.[114] A 2019 Department of Commerce report lists more than 60 recommendations; essentially all of them echo, and are nearly identical to, those made in previous similar reports from both Democratic and Republican administrations.[115] We have decades of nearly identical calls to action.[116] All of it distills to one essential directive: restructure the regulatory environment so that investors can open and operate domestic mines. There is one thing different today: the digital revolution now enables significant, and even radically new, possibilities for more cost-effective and environmentally gentle mineral extraction and production.

Significant advances are still possible in basic materials sciences and chemistry[117]—including techniques for reducing the use of hazardous chemicals needed for mineral refining and in recycling.[118] But, as with the industrial sector in general, it is in software domains where some of the greatest productivity and safety gains will be found.[119] Software and digital technology have finally improved sufficiently to begin offering the kinds of gains in “hard” industries, such as mining and manufacturing, as they have in “soft” industries such as news and entertainment.[120] Mines, for example, have only begun to use automated drills and trucks.[121]

Some intrepid entrepreneurs continue to advance mining development in the U.S., from the huge potential for copper, gold, and molybdenum in Alaska[122] to a rare earth deposit in Round Top, Texas,[123] and (also in Texas) the first non-China facility for refining rare earth ores.[124] The last, a joint venture between Australian, Japanese, and U.S. firms, had a planned start date in 2021.[125]

But in a sign of the times—and an illustration of the failure for green advocates to connect the dots to reality—when it was introduced last year, the administration’s proposal to expand domestic mining was met with partisan criticism as “shameful” and harmful to the environment.[126] But in calling for things like stockpiling (specifically for national defense), greater access to federal lands, financial support, and expedited permitting, today’s administration is following the same proposals made serially by previous administrations, in both political parties, over many decades.

Indeed, the administration’s call to action closely resembles legislation passed into law 40 years ago, on a bipartisan basis, and signed by President Carter. That law, the National Materials and Minerals Policy, Research and Development Act of 1980, specifically called for the coequal pursuit of mineral production and environmental protection.[127]

In order to provide the motivation and the expertise needed to reanimate domestic mining—an action that would provide benefits to all industries dependent on minerals—Congress should update the 1980 mining law. And new legislation should specifically include plans to:

- Resurrect the Bureau of Mines in order to provide an epicenter of expertise, now absent, needed to provide comprehensive, independent domain knowledge on mining technologies.

- Directly link all subsidies and mandates for green energy to policies that support the expansion of domestic mining and minerals refining.

Even without subsidies, mandates, and policies that favor green energy, the future for both America and the rest of the world will see many more wind and solar farms and many more electric cars. That will happen precisely because those technologies have matured enough to play significant roles. And given the magnitude of pent-up global demand for energy and energy-using machines and services—especially after the world struggles out of recession—it is a truth, not a slogan, that the world will need “all of the above” in energy supplies.

These realities, combined with the immutable reality that green machines require extraordinary quantities of energy minerals, can perhaps form a common intersection of interests that support an expansion in domestic mining. That would be, after all, of strategic and economic benefit to the United States, regardless of the debates over whether green energy is a replacement for hydrocarbons, which it is not, or a significant new and valuable energy sector, which it most assuredly is.

Endnotes

By Mark P. Mills

Source: Manhattan Institute