Caspian Games: Central Asian ‘stans’ Vie for Connectivity Market

Azerbaijan held a presidential election this month. Predictably, incumbent leader Ilham Aliyev won his fourth consecutive term with a Kim dynasty-esque 86% of the votes.

International monitors for the Organization for Security and Cooperation in Europe (OSCE) Office for Democratic Institutions and Human Rights (ODIHR) stressed “widespread disregard for mandatory procedures, numerous instances of serious irregularities and lack of transparency”; the Azeri electoral commission replied that such observations were “unfounded”.

Then the whole issue simply vanished. Why? Because, from a Western strategic perspective, Azerbaijan’s post-Soviet petro-autocracy is simply untouchable.

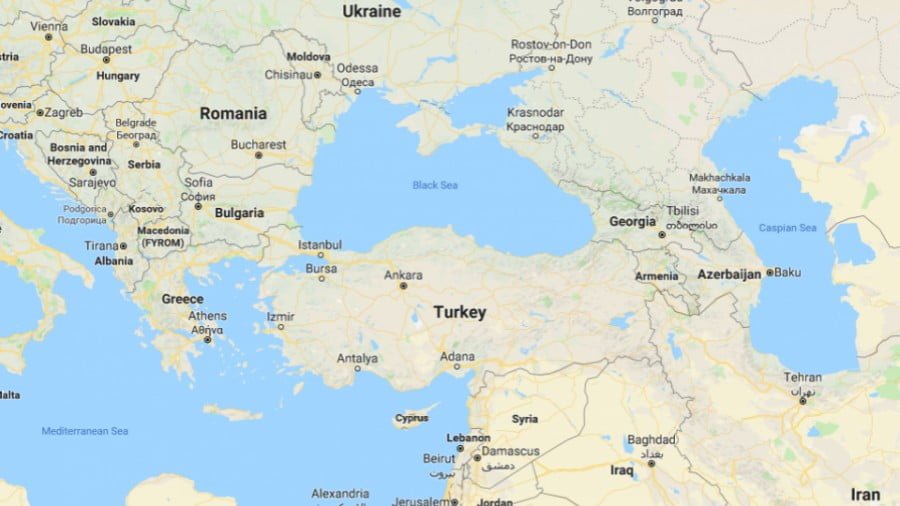

Much has to do with the Baku-Tblisi-Ceyhan (BTC) pipeline, facilitated by the late Zbigniew “Grand Chessboard” Brzezinski during the first Bill Clinton administration to bypass Iran. The BTC de facto unleashed the energy chapter of the New Great Game that I have called Pipelineistan.

Now, Baku is harboring great hopes for its new port at the desert wasteland of Alat (“Your hub in Eurasia!”), simultaneously connected to the West (Turkey and the European Union), the South (Iran and India) and the North (Russia).

Alat is also designed as a top logistics/manufacturing/connectivity hub of the New Silk Roads, aka Belt and Road Initiative. Its top strategic location straddles the BRI’s central connectivity corridor; links to the newly opened Baku-Tblisi-Kars railway, connecting the Caucasus with Central Asia; and also links with the International North-South Transport Corridor that connects Russia to India via Iran.

Transportation corridors are all the rage. For Azerbaijan, oil and gas may only last up to 2050. So the priority from now on is to engineer the transition toward becoming a logistics hub; actually, the premier Caspian Sea hub.

Do (Caspian) opposites attract?

Baku’s drive revisits and propels to the forefront the role of Pipelineistan and connectivity corridors in Eurasia integration. The overall picture may finally point to a “third way,” Europe-bound, for Caspian energy exports, for the moment mostly concentrated on Russia and China.

Turkmenistan is actively promoting itself this year as “the heart of the Great Silk Road.” Yet that’s centered more on reviving Ancient Silk Road sites than on digital connectivity.

Still, Ashgabat did anticipate the BRI when the 1,800-kilometer Central Asia-China gas pipeline, from Turkmenistan to Xinjiang via Uzbekistan and Kazakhstan, carrying 55 billion cubic meters (bcm) a year, was inaugurated in 2009.

Ashgabat and Moscow have had a tortuous spat that eventually led to Gazprom completely ceasing imports of Turkmen gas into Russia more than two years ago.

And that’s how Beijing, and not Moscow, ended up being configured as Central Asia’s top energy customer – and trading partner.

Because of its idiosyncratic practices, Turkmenistan in the end never managed to diversify its export markets. It operated the switch from Russia to China but could not land the lucrative European market.

It has been a mantra in Brussels for ages now that the EU needs energy diversification away from Gazprom – even as member nations are incapable of agreeing on the mere lineaments of a common energy policy.

European companies at best are developing major oilfields in Kazakhstan. But on the “blue gold” Pipelineistan front, so far no gas from Central Asia is flowing to Europe.

The traumatic experiences of the past are epitomized by the Nabucco soap opera – a pipeline from Turkmenistan via the Caspian to Turkey and beyond that in the end will never be built.

Azerbaijan and Turkmenistan are actually stiff competitors on opposite shores of the Caspian. Baku was delighted with Nabucco’s failure because that boosted the prospects of its own gas from the sprawling Shah Deniz field hitting Europe. The key Nabucco problem was the mystery surrounding Turkmenistan’s real gas-production capability, considering that most of its gas is now directed toward China.

A complicating factor is that any pipeline that crosses the still legally undefined Caspian (is it a sea or is it a lake?) is also not exactly welcomed by either Russia or Iran.

Gazprom has its own plans to increase its share of the European market via Nord Stream and Turk Stream. Iran would aim finally to crack European markets via a possible pipeline from the massive South Pars field in cooperation with Qatar, a revamped version of the Iran-Iraq-Syria pipeline that was one of the key reasons for the war in Syria.

TAP meets TANAP

So in the end the only realistic Pipelineistan gambit in terms of Caspian gas connections to European markets is bound to be the small, €4,5 billion (US$5.55 billion) Trans-Adriatic Pipeline (TAP), carrying 10bcm of gas a year from Baku.

TAP, only 878km long (northern Greece 550km; Albania 215km; Adriatic Sea 105km; southern Italy 8km), is supposed to come online by March 2020.

TAP will be a sort of extension of the way more ambitious, $8 billion Trans-Anatolian Natural Gas Pipeline (TANAP), which will ship gas from Azerbaijan’s Shah Deniz 2 to western Turkey, as configured by the so-called Southern Gas Corridor. TAP and TANAP will connect at the Greek-Turkish border.

It’s enlightening to compare how Azerbaijan is betting on Europe while Turkmenistan bets on China.

And then there’s Kazakhstan – which deploys its own, branded, “multi-vector” foreign policy involving Russia, China, the US and the EU.

At the same time that Astana is a key node of the BRI, a member of the Eurasian Economic Union (EEU) and a member of the Shanghai Cooperation Organization (SCO), it welcomes investment from EU majors and US oil giants.

Going forward, the trend is Beijing enjoying a strategic advantage as the top trading partner of every Central Asian “stan” except Kazakhstan, while Moscow maintains its multiple roles as security provider, trading partner, source of foreign investment, employer to millions of Central Asian expats, and Soft Power Central (Russian is the lingua franca in Central Asia, and Russian TV and culture are ubiquitous).

And this will all play within the framework of interpolation between BRI and the EEU.

But what about Iran and Turkey in the Big Picture?

Azerbaijan, as a Caspian nation, maintains deep ethnic and linguistic links with Turkey. Yet Baku prizes secularism in an Ataturk vein – which sets it at odds with Turkish President Recep Tayyip Erdogan’s Islamic-tinged neo-Ottomanism.

The major complicating factor is that Ankara and Moscow are collaborating on Turk Stream – in essence a Pipelineistan move from Siberia to Europe under the Black Sea directly competing with Azerbaijan’s own gas exports.

Iran for its part deploys ample cultural and linguistic influence all across Central Asia. In fact Persia, historically, has been the top organizing entity across Central Asia. Iran is as much a Central Asian power as Southwest Asian (what the west calls the Middle East).

But in a BRI environment shaped by the building of roads, railways, bridges, tunnels, pipelines, and fiber-optic networks, the real game-changing player in Central Asia will continue to be China – allegedly more than Turkey, Iran and Russia.

Chinese companies already own roughly 25% of Kazakhstan’s oil production and practically all of Turkmenistan’s gas exports. And they have their sights on Baku as a major BRI node.

Call it a sort of digital revival of the Tang dynasty, when Chinese imperial influence extended across Central Asia all the way to northeastern Iran. Any bets on the Caspian soon becoming a Chinese lake?