The Journey to Monetary Gold and Silver

Markets are just beginning to latch on to the economic consequences of the coronavirus. Central banks are slashing interest rates and beginning to throw new money into the mix and governments are increasing deficit spending.

Few analysts have yet to understand the enormous consequences of the coronavirus for missed payments and accumulating current debt, which is and will rapidly drain liquidity from wholesale money markets. It is increasingly certain that the eurozone’s banking system will require rescuing from insolvency with knock-on consequences for the global monetary system. Concern over the consequences for the $640 trillion OTC notional derivative market, particularly for $26 trillion of fx swaps, is so far absent.

Continuing on our theme that the fates of the dollar and US Treasury values are closely bound, the extraordinary overvaluation of the bond market will translate into a collapse for both. This article charts how the collapse of the dollar and financial asset values is likely to progress and concludes that we are witnessing the end of the neo-Keynesian fiat currency fantasy, which will be done and dusted with surprising rapidity.

Only then will sound money, after varying time periods for different nations, return.

Setting the scene…

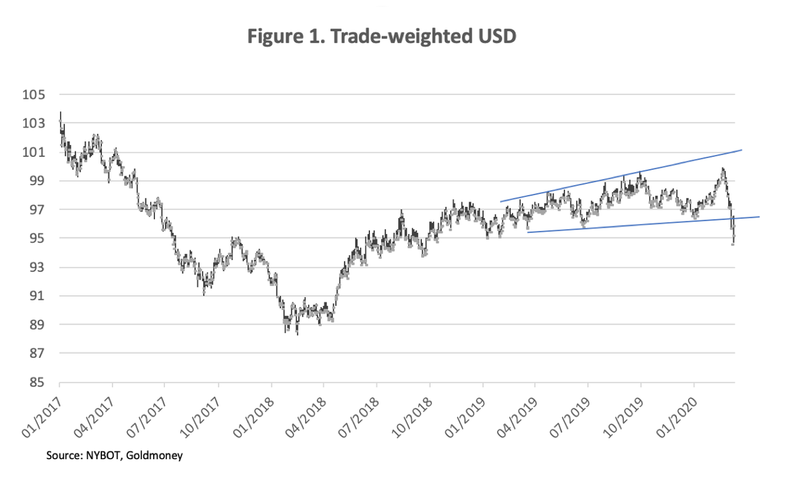

This week we got into the red meat of Scene One of the final Act of the financial tragedy currently staged in global markets. It is a drama that has run on the air of hope for a hundred years, with an ending that now appears to be unexpectedly sudden. We face no less than the destruction of a financial system whose twin pillars are fiat currencies and financial assets, built on the sands of monetary expansion and debt financing. The evidence of its commencement is best encapsulated in Figure 1, of the world’s reserve currency. This is where everyone was meant to seek sanctuary from lesser currencies, in order to have the liquidity to pay the coupons on their dollar debts.

It is turning out not to be so, with the dollar suddenly appearing to enter a new bear market. Meanwhile, this week saw the entire US Treasury yield curve briefly submerged under 1%, an event bifurcated from the collapsing dollar.

There is no doubt that the coronavirus is having a serious economic impact. Much has been written about the disruption of supply chains, and clearly people are staying at home and stockpiling necessities. Sales of automobiles and other durable goods have crashed. Now the politicians are falling ill. Investors have reacted by dumping equities and buying government bonds, a flight to safety by Keynesian investment managers seeking the comfort of Nurse for fear of something worse. Consequently, government bond prices have become even more detached from the true reality of where financial risk resides.

Amazingly, almost no investment manager has bought physical gold for his or her clients: gold-backed ETFs and derivatives are only paper claims on gold, so by having counterparty risk and the lack of true possession don’t count as true safety. Physical gold has been effectively banned from managed portfolios, being classified as unregulated, deterring investment managers from having to justify buying gold to their compliance officers. The related asset class is so downgraded that gold and silver mining shares remain unfashionable, with the Amex gold bugs index (HUI) standing at about one third of its 2011 peak while the gold price is in new high ground against nearly all fiat currencies.

Monetary debasement will really accelerate from here…

Monetary and market distortions could have persisted for longer if it were not for the fact that the coronavirus disruption is accompanied by considerable payment dislocation. Companies still have fixed costs when they have no sales, either because customers are not turning up or their supply chains have stopped delivering products. Where companies have cash at their banks, they will draw it down, forcing their banks to go into the money markets, either through LIBOR or repos to make up the balance, sell government bonds, or foreclose on borrowers. Where companies do not have cash, they will test their working capital facilities, likely to force their banks to cover increased lending in wholesale money markets. Where banks experience drawdowns on both sides of their balance sheets, outstanding bank credit contracts, sending the sort of signal that terrifies central bankers.

The situation will be increasingly reflected by central banks having to back-stop both liquidity and bank reserves through repos and new rounds of quantitative easing. In an interesting paper, Zoltan Pozsar of Credit Suisse describes the process that leads to what he terms deficit agents in supply chains (businesses experiencing payment failures) turning their banks into deficit agents as well.

Pozsar demonstrates that a reluctant Fed will have to backstop not just escalating domestic dollar deficits but global ones as well, and he assumes for the purpose of clarity that foreign central banks will manage the payment crises in their own currencies. Being a money market technician, he does not address the debasement issue because that is not his brief. But clearly, he describes a process where the dollar will have to be debased if financial asset values, particularly of government bonds, are to be maintained.

We see unfolding the process whereby both the dollar and financial assets are losing value, with the dollar losing it first. And while a weakening dollar may from time to time lend support to financial asset prices, measured in sound money their combined values will decline.

The second scene in the final act of our financial tragedy will be wholesale liquidation of US Treasury holdings by banks in New York and also by foreign governments to obtain dollars to satisfy their liquidity demands. The Fed will have to supply as much liquidity as it takes to accommodate the American banks and will reduce the Fed funds rate to discourage them from selling Treasury bills and bonds. As for foreigners, they are not the Fed’s first priority.

Let us assume liquidity problems should not become acute for the few foreign central banks with existing USD liquidity swap lines with the Fed. Under the existing 2013 agreement, these are only the ECB, Bank of England, Swiss National Bank, Bank of Canada and Bank of Japan. While additional temporary swap agreements might be arranged with others, it is only likely to happen in a response to liquidity stresses rather than in anticipation.

China, Korea and Taiwan as well as other nations with dollar-centric supply chains in their domains will probably have to unwind their long-dollar fx swap positions and sell T-bills and Treasuries in order to release the necessary liquidity. The end result is that in funding the US deficit, the Fed will have to not only absorb significant new debt through quantitative easing, but it will have to buy up existing debt sold by foreign holders if it is to maintain US Treasury yields at anything like current levels.

In this, mainstream opinion has been wrongfooted: foreigners certainly have dollar obligations to satisfy in an economic slump, but they already own the dollars. The thirst of foreigners for dollar liquidity will not be satisfied by the purchase of more dollars, but by the liquidation of their existing dollar assets. And to the extent that this leads to a contraction in bank credit the Fed will have no alternative but to sacrifice the dollar by increasing the base money quantity in order to absorb it all.

Furthermore, there is an unknown quantity of fx swaps taken out by US hedge funds to strip out interest rate differentials between euros and yen on one side, and the dollar on the other. It is a trade that will have built in quantity but deteriorating in quality since April 2018, when it first became clear to American based investors and speculators that the euro and yen were seemingly stuck with negative interest rates in perpetuity, while the Trump stimulus would likely lead to higher dollar rates. Now that the Fed is closing down the rate differential by cutting its funds rate these arbitrages need to be unwound, leading to substantial liquidation of T-bills, USTs and dollars to repay obligations in euros and yen. No wonder the chart of the dollar’s trade weighted index is so bearish.

Hopefully, the hedge fund problem will not replicate the crisis in September 1998, when the Long-Term Capital Management hedge fund failed. But even if that risk is contained, there will be a significant contraction of outstanding bank credit in dollar markets. Being sold on Irving Fisher’s description of how contracting bank credit led to the 1930s depression, the Fed is likely to respond by turning its liquidity taps full on.

The fiscal position is not good either. The current year US budget deficit, estimated by the CBO to be over a trillion dollars, will begin to look like running at an annualised rate of nearly twice that. The Fed could also find itself monetising not only the bulk of new Treasury flows but absorbing sales by foreigners of UST bonds, T-bills and agency debt as well. If so, it will end up increasing its balance sheet by many trillions, unless, that is, the Fed adjusts its priorities to protect the dollar. But the cost of doing so would be the inevitable destruction of US Government finances when the Fed refuses to monetise its debt. That simply won’t happen.

The sacrifice of the dollar as the Fed inevitably fails to maintain financial asset values will truly mark the end of the fiat currency era, since no other fiat currency can exist with the world’s reserve currency thoroughly debased and its financial assets in a state of collapse. This is a simple statement with complex issues behind it, including but not limited to the following:

- The valuations placed on government bonds are so divorced from economic reality that after the initial shock in equity markets has passed, they will be exposed to a seismic downwards adjustment in prices.

- Corporate bond markets will face an even greater collapse as risk premiums widen, leading to a spate of bankruptcies in the private sector and losses on collateralised loan obligations held by the banks on a systemically threatening scale.

- Hedge funds which have taken out fx swaps have already lost the interest rate arbitrage opportunity following the Fed’s recent cut in the funds rate. Furthermore, with T-bills yielding only 0.37%, further cuts in the funds rate are a racing certainty. Unwinding these fx swaps is one factor that will put significant downward pressure on the dollar.

- A reduction in outstanding derivatives will be the consequence of banks desperate to free up liquidity for their own balance sheets. The cost of hedging risk will increase significantly and in many instances become unavailable. Hedge funds and the like will be forced to restrict their activities, raising the possibility of widespread losses and potential failures in financial asset markets.

- A glance at their share prices confirms that major European banks are already in trouble and they have long been at severe risk of failure, a fact which has been concealed by the ECB’s provision of liquidity. If nothing else, a new escalation of non-performing loans brought about by the coronavirus now threatens to collapse Italian, French, German, Spanish and other eurozone nations’ commercial banks despite the ECB’s efforts. A coordinated G-20 global bank rescue scheme involving open-ended monetary expansion by central banks is likely to be instigated in a widespread act of currency inflation.

- A general liquidation of foreign-owned dollar assets and selling of dollars is likely to follow.

- Only then will the wider public begin to realise the full faith and credit in their governments and currencies which they take for granted are worthless.

The confluence of these threats to financial assets and the world’s reserve currency makes it almost certain that this time attempts to rescue the world from another financial crisis will fail. The twin pillars in the Keynesian endgame, whereby the future of financial assets has become tightly bound to the purchasing power of currencies, will both be destroyed by market forces acting like Sampson pushing the pillars apart until the temple’s collapse killed all the Philistines.

Comparing fiat to sound money

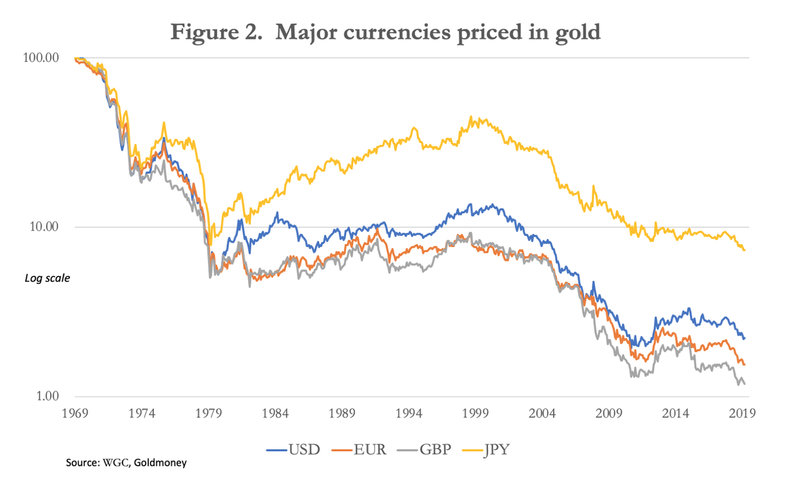

Figure 2 shows that since the gold pool failed in the late 1960s the four major currencies (including the euro’s components prior to 1999) have lost substantially all of their purchasing power, compared with that of gold. The most debased is sterling, which retains only 1.19% of its 1969 purchasing power, followed by the euro at 1.56%, the dollar at 2.22% and the yen at 7.4%.

The failure of the gold pool and the subsequent abandonment of the post-war Bretton Woods agreement was the last significant monetary failure. The first in modern times was the 1934 devaluation of the dollar from $20.67 to $35 per ounce of gold, thirty-five years before. On this timeline the next failure appears to be overdue.

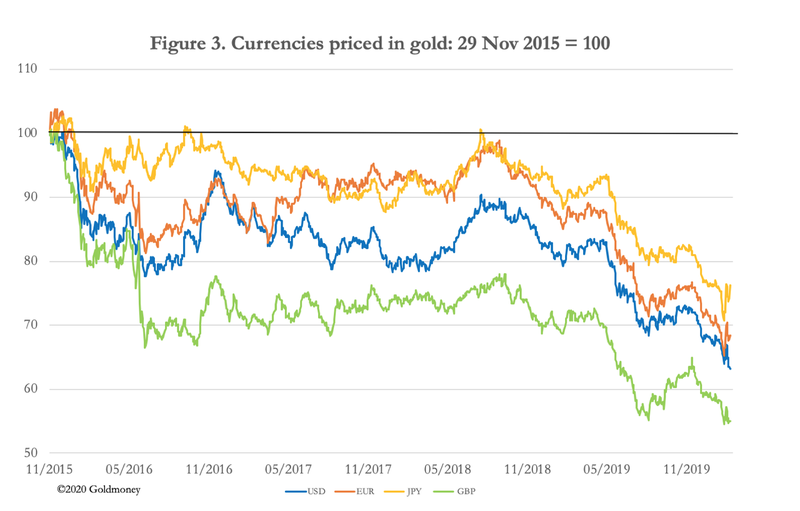

The current situation has the makings of leading into an even greater monetary event, as government spending spirals beyond control without the means to fund it, except by monetary inflation. It has already been anticipated by a renewal in the bear market in the major currencies measured in gold terms, dating from late-2015 and is illustrated in Figure 3.

These represent significant losses ahead of the currency debasement which is now becoming increasingly certain in the coming months. It is extraordinary that this marked devaluation of currencies has occurred with very few commentators noticing.

If we refer back to John Law’s Mississippi bubble, which is the best model for what is now unfolding, the loss of all purchasing power for his fiat currency happened in less than a year. Law’s livre began the final phase of its decline in November or December 1719 and by the following September there was no exchange rate against sterling, indicating it was worthless. From November 1719 Law accelerated his purchases of shares in his Mississippi venture ahead of its merger with his bank, the Banque Royale, paid for by issuing unbacked paper livres which began to noticeably undermine its purchasing power.

Sticking with Law’s failure as a template for ours today, we can similarly expect the Fed on behalf of the US Government to issue new money for the purpose of maintaining financial asset values, mainly of US Treasury bonds, but by extension of equity prices as well.

Following the current panic into perceived safety, a second phase will likely evolve, being driven by the collapse of government bond prices. Currently, they are over-valued on a combination of unrecognised price inflation, which based on independent estimates is probably closer to ten per cent than two, and a flight to perceived safety from other financial assets. That process will come to an end, and the condition of government finances, which ultimately depend upon the wealth and health of the productive economy, are bound to be reassessed in the light of the slump in business activity and a more realistic assessment of price inflation.

To sum up, the following developments are likely in the coming months in approximate order, with some running concurrently:

- Base money will be increased substantially to offset a contraction in bank credit and to give banks extra liquidity to compensate for becoming deficit agents as supply chains dislocate and retail sales of non-essentials goods and services collapse. We have already seen daily repos by the Fed increasing from about $40bn in recent weeks to between $130bn to $200bn currently.

- “Helicopter money” in various guises, such as deferral of tax payments and business rates to help provide liquidity, will shift to governments some of the deficits building up in businesses. Mortgage payment holidays are offered in some countries. Helicopter money is already being provided to investors through share support operations, such as the Bank of Japan’s purchases of ETFs, which is likely to be expanded. In Hong Kong, each citizen is being given HK$10,000.

- Within a month or two there will almost certainly have to be bank bailouts in Europe, which will require additional monetary commitments by the ECB and the national central banks. This will likely lead in turn to widespread liquidation of euro commitments for speculation and arbitrage. Loans in the trillions have been taken out in euros as the counterpart in fx swaps to the dollar. As these positions are squared the euro will rise and the dollar will fall, transmitting a eurozone banking crisis into liquidation of UST-bills and short-term US Government coupon debt by US hedge funds. A heightened risk of counterparty failure in fx swaps could spread to other derivative markets, requiring bailouts of non-banks, including major hedge funds. Failure to do so or a bungled operation such as tinkering with mandated bail-ins could hasten the collapse of stocks and other financial assets.

- A declining dollar will increase portfolio liquidation pressures on foreigners, leading to indiscriminate offerings of US Treasuries, agency debt and equities. The Fed will have to take on not only the financing of an increasing budget deficit, but also absorb foreign sales of dollar-denominated securities if it is to retain control of prices.

- At this stage it will become increasingly obvious to domestic bank deposit holders that the dollar’s purchasing power is being destroyed by the Fed’s escalating asset support commitments. In effect, the Fed will be the only significant buyer of financial assets, paid for through quantitative easing on a far greater scale than that which followed the Lehman crisis.

- In the absence of other buyers of US Treasuries and the loss of purchasing power for the dollar, bond prices will sink, which will make it virtually impossible for the US Treasury to fund a ballooning deficit. An election year creates extra difficulties leading to uncertain political outcomes. But by the time President Trump is due to stand for re-election, over a million elderly and poor Americans might have died from the coronavirus, socialist Democrats might be in the ascendant and the dollar could become worthless.

- With the dollar as the world’s reserve currency and nearly all other fiat currencies having taken their cue from it since the Nixon shock in 1971, they also seem doomed to failure with the dollar.

Where will the money go?

In the three months before the collapse of his scheme, sellers of shares in his Mississippi venture required John Law to replace them with new buyers, and when they could not be found he substituted them by buying shares with new livres issued for the purpose. Today’s price support system which rigs government bond prices is exactly the same concept as that deployed by John Law, except it is on a global scale.

Law’s experience showed that in an asset and monetary collapse, apparent wealth simply vanishes, destroyed along with the medium of exchange. Theoretically, if there are no buyers at any price the collapse to zero is immediate and no one extracts any value to be redeployed elsewhere. The Mississippi bubble also showed that the purchasing power of sound money, always gold or silver, is at least retained. For this reason, it is more than likely a rising price for monetary gold will happen without very much gold needing to be purchased.

Being dominated by mathematical economists, current thinking in financial asset markets does not often admit to this. But as the central banks show increasing difficulty in maintaining the combined values of currency and bonds, the price of gold and silver in fiat currency terms will rise significantly. More correctly described, the ratios of fiat currencies to gold will fall, as illustrated in Figures 2 and 3 above.

Gold and silver are reliable money, chosen by the people as economic actors. The journey to their reinstatement will require the destruction of the unsound currency issued by the state, which is simply a distorting monopolist and therefore a distorter and destroyer of economic values. Only then can gold and silver re-emerge as circulating money, or more practically, reliable and trusted paper and electronic substitutes for them. Gold and silver are emblems of economic freedom, and while the transition will only be very reluctantly accepted by the state, a better monetary future will beckon.

It is in this light we should anticipate the money to replace dollars, euros, yen and pounds. In Asia they will be better placed than western nations to return to sound money, with Russia having substantially replaced its reserve dollars with gold, which could easily be legislated into a gold exchange standard for the rouble. China will be in a position to do the same for the yuan. In theory, getting to the point where monetary stability returns will be easier for some governments than for others. The capitalist nations, and China perhaps to a lesser extent, have subsumed Keynesian economics deep into their collective psyche, so deep that it has replaced entirely an understanding of free market economics.

Governments with extensive welfare obligations will find it an enormous challenge to maintain the balanced budgets required to ensure that a new monetary system will endure. They have been socialising wealth for too long to understand the simple fact that if you wish your nation to be prosperous you must allow the people to create and retain it. You must also make them responsible for their own affairs and make it clear to them that no one individual, lobbyist or interest has a right to government intervention. The function of government must be limited to making and administering criminal and contract law and protecting the realm, with strictly limited welfare provision.

A government that works in a sound money environment absorbs and administers only a minor part of its national economy. The loss of political power is always widely resisted, but the redeployment of national resources from a wealth-destroying state to free-market production has been shown to produce remarkable benefits in surprisingly little time. If, that is, the political class is wisely led by statesmen not in thrall to the common economic fallacies of John Maynard Keynes and John Law.

By Alasdair Macleod

Source: Gold Money